What the Heck is Accrual Accounting and Why Does it Matter?

Accrual…what?

If you didn’t have the pleasure of attending business or accounting school, it’s understandable that some of the accounting jargon can leave you feeling confused.

But accrual accounting isn’t a small definition at the back of an accounting textbook. Choosing accrual accounting can be the foundation for how you set up your entire bookkeeping and accounting systems, positioning you for success.

Shall we get into it?

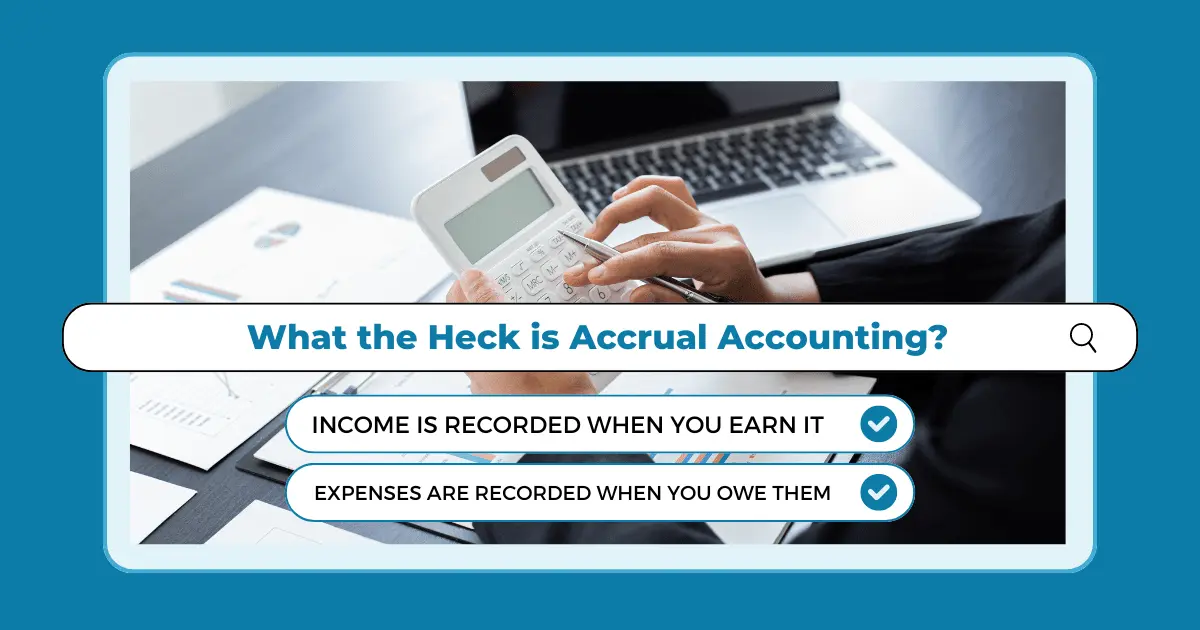

So, What the Heck is Accrual Accounting?

In plain English, accrual accounting is all about timing.

It’s a method where you record income and expenses when they’re earned or incurred, not necessarily when the cash changes hands.

- Income is recorded when you earn it, like when you send out an invoice, even if your customer hasn’t paid yet.

- Expenses are recorded when you owe them, such as when you receive a bill, not just when you actually pay it.

Accrual accounting gives you credit for being productive, not just for having money in the bank. It’s like recognizing that you’ve run a marathon, even if you haven’t collected all your medals yet!

Who the Heck Cares About Accrual Accounting?

Glad you asked!

Accrual accounting gives you a more accurate and realistic picture of your business’s financial health.

Most businesses opt for accrual accounting, and most accounting and finance professionals recommend considering this method.

Here’s why:

- Big Picture View: It shows you the true financial performance of your business over a period of time. You’re matching revenues to the expenses incurred to generate them, which makes your financial statements more meaningful.

- Plan Ahead: By recognizing income and expenses when they happen, you can better predict future cash flows, helping you plan for upcoming expenses or investments.

- Trustworthy Reports: Lenders, investors, and stakeholders prefer accrual accounting because it provides a clearer picture of your company’s financial position.

If you’re working on a big project that spans several months, accrual accounting helps you recognize portions of the revenue and expenses as you progress, giving you a real-time view of how profitable the project is at any given moment.

When The Heck Should a Business Use Accrual Accounting?

If you’re a small business just starting out, cash accounting might seem easier. In these cases, you simply record transactions whenever cash changes hands.

But as your business grows, accrual accounting becomes more beneficial—and sometimes necessary.

Consider using accrual accounting if:

-

- You Deal with Large Projects or Contracts: If you provide services or products over time, accrual accounting helps you match income and expenses accurately.

- You Offer Credit to Customers: Recording sales when you invoice (not just when you get paid) gives you a better handle on revenues and outstanding receivables.

- You’re Seeking Funding or Investors: Accrual-based financial statements are generally required by banks and investors because they reflect your business’s true financial performance.

- You Have Plans for Revenue Growth: If large income growth is on the horizon, accrual accounting is generally recommended.

- The IRS Requires It: C corporations and those partnering with a C corporation partner are generally required to use accrual accounting. Also, most entities engaging in “the production, purchase, or sale of merchandise as an income-producing factor” should use accrual accounting for inventory transactions at least.

- You Deal with Large Projects or Contracts: If you provide services or products over time, accrual accounting helps you match income and expenses accurately.

But Wait, What’s the Catch?

Like anything worthwhile, accrual accounting isn’t without its challenges.

- Complexity: It’s more complicated than cash accounting. You’ll need to track receivables and payables diligently.

- Cash Flow Confusion: You might show a profit on your income statement while your bank account is running on fumes. That’s because accrual accounting recognizes revenue you’ve earned but not yet received.

- More Effort: It requires more accurate record-keeping and a solid accounting system to manage it effectively.

But don’t let that scare you off! The benefits often outweigh the extra effort, especially when you have the right support.

3 Key Takeaways

Accrual accounting is the recommended way to go for most up-and-coming businesses. Despite a bit of extra work, at New Economy we encourage our clients to use accrual accounting for their businesses to ensure they’re ready to crush their goals.

Remember:

- Accrual = Accuracy: It provides a clearer, more accurate view of your business’s finances by matching income and expenses when they occur.

- Growth-Ready: If your business is scaling, accrual accounting helps you track financial performance more effectively, making it easier to plan and secure funding.

- Support is Key: The complexity of accrual accounting is manageable with the right help. Partnering with experts like New Economy ensures you get the benefits without the headaches.

There you have it 🙂

How New Economy Can Help

Switching to accrual accounting might feel like you’re learning a new language, but our team is fluent in and can be your translator.

At New Economy, we’re pros at helping businesses make the transition smoothly.

- Expert Guidance: We’ll help set up your accounting system so that it’s tailored to your business needs.

- Ongoing Support: Our team provides continuous assistance, ensuring your financial records are accurate and up-to-date.

- Customized Reporting: We make sense of the numbers, providing reports that are easy to understand and actionable.

Schedule a time to meet with our Founder, Jeff, so we can take care of the accrual accounting stuff for you!