If you didn’t have the pleasure of attending business or accounting school, it’s understandable that some of the accounting jargon can leave you feeling confused.

But accrual accounting isn’t a small definition at the back of an accounting textbook. Choosing accrual accounting can be the foundation for how you set up your entire bookkeeping and accounting systems, positioning you for success.

Shall we get into it?

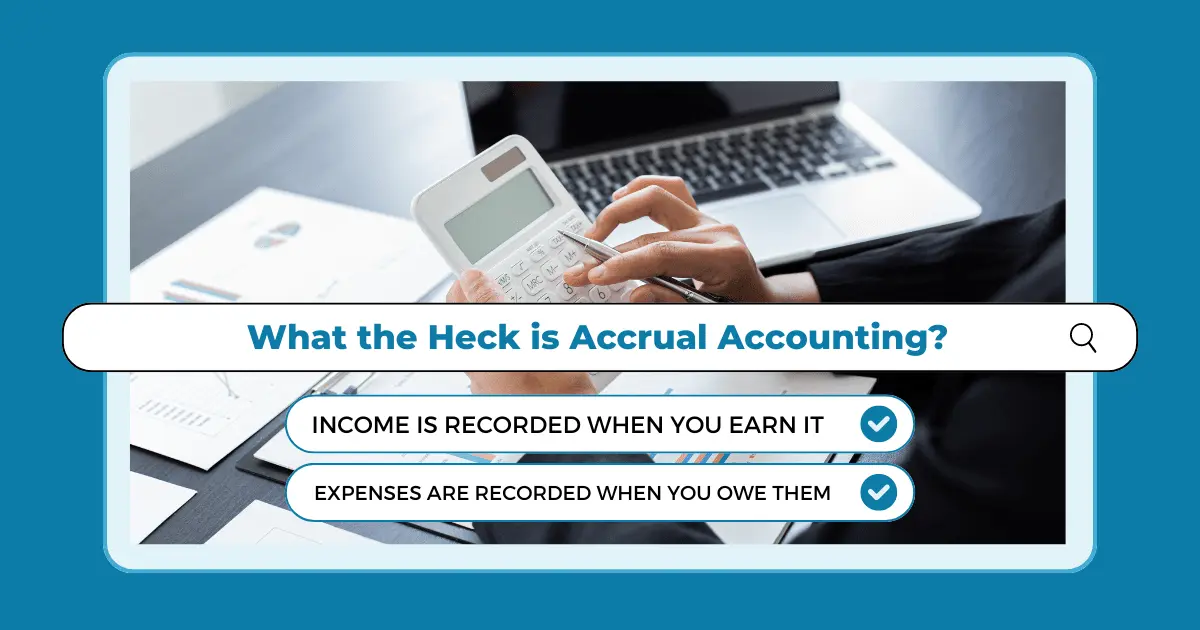

So, What the Heck is Accrual Accounting?

In plain English, accrual accounting is all about timing.

It’s a method where you record income and expenses when they’re earned or incurred, not necessarily when the cash changes hands.

Income is recorded when you earn it, like when you send out an invoice, even if your customer hasn’t paid yet.

Expenses are recorded when you owe them, such as when you receive a bill, not just when you actually pay it.

Accrual accounting gives you credit for being productive, not just for having money in the bank. It’s like recognizing that you’ve run a marathon, even if you haven’t collected all your medals yet!

Who the Heck Cares About Accrual Accounting?

Glad you asked!

Accrual accounting gives you a more accurate and realistic picture of your business’s financial health.

Big Picture View: It shows you the true financial performance of your business over a period of time. You’re matching revenues to the expenses incurred to generate them, which makes your financial statements more meaningful.

Plan Ahead: By recognizing income and expenses when they happen, you can better predict future cash flows, helping you plan for upcoming expenses or investments.

Trustworthy Reports: Lenders, investors, and stakeholders prefer accrual accounting because it provides a clearer picture of your company’s financial position.

If you’re working on a big project that spans several months, accrual accounting helps you recognize portions of the revenue and expenses as you progress, giving you a real-time view of how profitable the project is at any given moment.

When The Heck Should a Business Use Accrual Accounting?

If you’re a small business just starting out, cash accounting might seem easier. In these cases, you simply record transactions whenever cash changes hands.

But as your business grows, accrual accounting becomes more beneficial—and sometimes necessary.

Consider using accrual accounting if:

You Deal with Large Projects or Contracts: If you provide services or products over time, accrual accounting helps you match income and expenses accurately.

You Offer Credit to Customers: Recording sales when you invoice (not just when you get paid) gives you a better handle on revenues and outstanding receivables.

You’re Seeking Funding or Investors: Accrual-based financial statements are generally required by banks and investors because they reflect your business’s true financial performance.

You Have Plans for Revenue Growth: If large income growth is on the horizon, accrual accounting is generally recommended.

The IRS Requires It: C corporations and those partnering with a C corporation partner are generally required to use accrual accounting. Also, most entities engaging in “the production, purchase, or sale of merchandise as an income-producing factor” should use accrual accounting for inventory transactions at least.

But Wait, What’s the Catch?

Like anything worthwhile, accrual accounting isn’t without its challenges.

Complexity: It’s more complicated than cash accounting. You’ll need to track receivables and payables diligently.

Cash Flow Confusion: You might show a profit on your income statement while your bank account is running on fumes. That’s because accrual accounting recognizes revenue you’ve earned but not yet received.

More Effort: It requires more accurate record-keeping and a solid accounting system to manage it effectively.

But don’t let that scare you off! The benefits often outweigh the extra effort, especially when you have the right support.

3 Key Takeaways

Accrual accounting is the recommended way to go for most up-and-coming businesses. Despite a bit of extra work, at New Economy we encourage our clients to use accrual accounting for their businesses to ensure they’re ready to crush their goals.

Remember:

Accrual = Accuracy: It provides a clearer, more accurate view of your business’s finances by matching income and expenses when they occur.

Growth-Ready: If your business is scaling, accrual accounting helps you track financial performance more effectively, making it easier to plan and secure funding.

https://neweconomycpa.com/wp-content/uploads/2024/09/New-Economy-1.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-09-23 12:19:412024-09-23 16:29:30What the Heck is Accrual Accounting and Why Does it Matter?

Do you ever dread talking with your accounting team?

Do you finish conversations with your accountant feeling more confused than confident?

Do your finances feel more like a mystery than a roadmap?

I hate to break it to you…but your accounting team might suck.

We get it—“sucks” might sound harsh.

We’re accountants too, and we’ve met some amazing accountants along the way (many who we hired for our team!)

But too often we’ve found many CPAs who are doing a massive disservice to businesses, and it doesn’t have to be that way.

Sometimes it’s a lack of training, communication skills, or resources. But whatever the reason for this predicament, it’s better to figure it out sooner rather than later.

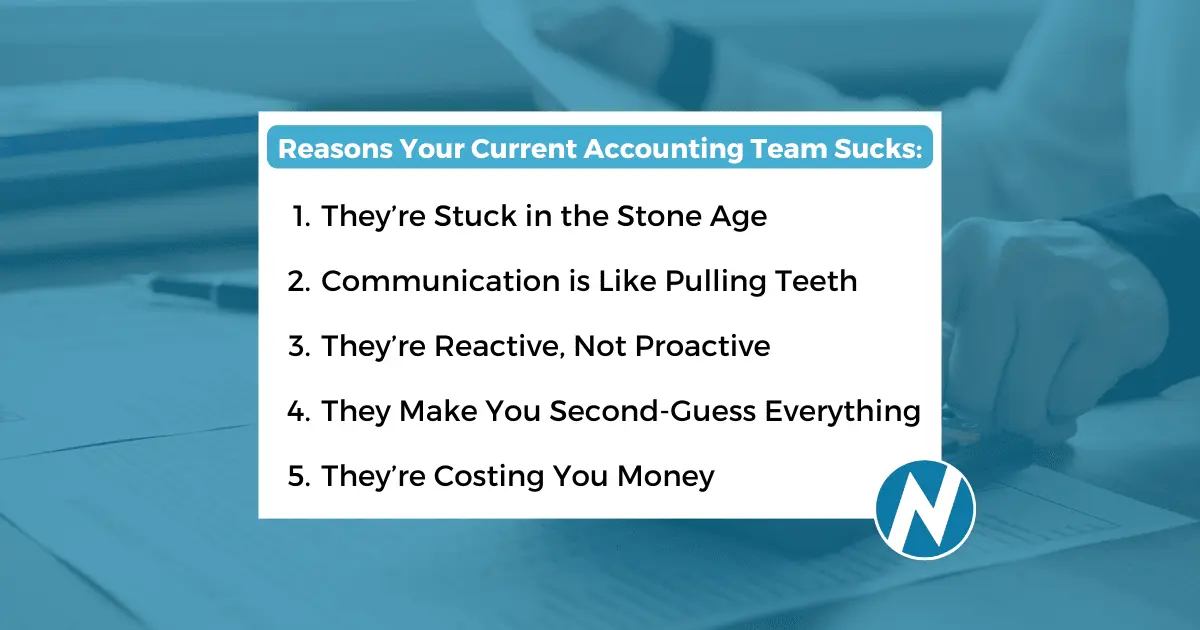

If your accounting team is still relying on endless spreadsheets, manual entries, and outdated software, you’re dealing with a serious case of inefficiency.

Spreadsheets have their place, but they’re not meant to be the backbone of your financial operations. Outdated tools mean higher chances of errors, slower processes, and more time spent on tasks that could be automated.

The Math on Why it Sucks:

Manual data entry = more errors

Outdated software = missed opportunities for efficiency

Time wasted on repetitive tasks = less time for strategy

What You Deserve: A modern accounting team should be using up-to-date software and automation tools to streamline processes, reduce errors, and save time.

2. Communication is Like Pulling Teeth

Does Your Team Only Speak Numbers?

Financial reports filled with jargon, explanations that leave you more confused, and updates that are as clear as mud—these are all signs of poor communication.

If you can’t understand what your numbers are telling you, how are you supposed to make informed decisions?

Lack of clarity = lack of confidence in your financials

What You Deserve: Your accounting team should be able to break down complex financial concepts into simple understandable language. You shouldn’t need a degree in finance to know where your money is going. Clear, jargon-free communication helps you stay informed and confident in your decisions.

3. They’re Reactive, Not Proactive

Always Playing Catch-Up?

Is your accounting team constantly putting out fires instead of preventing them? A reactive approach means they’re only dealing with problems as they arise—missing out on opportunities to optimize and plan for the future.

It’s like driving while only looking in the rearview mirror. Sure, you’ll see what’s behind you, but you’re likely to miss what’s up ahead.

The Math on Why it Sucks:

Constantly scrambling to fix issues = Missed opportunities for growth + savings

What You Deserve: A proactive accounting team doesn’t wait for problems to arise—they anticipate them and take action to prevent them. Regular financial reviews, strategic planning, and forward-thinking advice keep your business ahead of the curve. Your team will ideally always be one step ahead, so you can focus on running and growing your business.

4. They Make You Second-Guess Everything

Confidence in the Red?

If your accounting team isn’t providing you with clear, accurate information, it’s easy to start second-guessing every decision you make. Maybe you’re not sure if your financials are accurate, or you’re uncertain about the reports you’re getting.

When you don’t trust the numbers, it’s hard to move forward with confidence.

The Math on Why it Sucks:

Doubt in your financials = indecision

Second-guessing your strategy = missed opportunities

Constant worry about mistakes = more stress

What You Deserve: A solid accounting team provides you with clarity and assurance, turning uncertainty into confidence. With accurate reports and expert advice, you can make informed decisions without the constant fear of making a mistake. It’s about transforming your financials from a source of stress into a powerful tool for growth.

5. They’re Costing You Money

Financial Errors and Missed Opportunities

Errors in accounting aren’t just annoying—they can be downright expensive. Whether it’s overpaying on taxes, missing out on deductions, or dealing with mistakes that lead to penalties, a subpar accounting team can take a serious toll on your bottom line.

The Math on Why it Sucks:

Overpaid taxes = money out the window

Missed deductions and credits = lost opportunities

Penalties and fees due to errors = unnecessary costs

What You Deserve: An accounting team that’s meticulous and knowledgeable, ensuring that your finances are optimized. They should be spotting every deduction, maximizing your tax benefits, and catching errors before they become costly problems.

You Deserve an Accounting and Finance Team that Rocks

The right accounting team doesn’t just help you avoid pain, they create a solid foundation for growth. They can turn your financial operations into a source of strength, not stress.

If your current team is stuck in the past, poor at communication, reactive instead of proactive, making you second-guess everything, and costing you money, it’s time to reconsider your options.

So, take a step back, evaluate your current team, and don’t be afraid to make a change if it’s needed. Your business—and your peace of mind—are worth it.

3 Key Takeaways:

At New Economy, we take pride in helping our clients find accounting solutions that don’t suck. In fact, we might even find solutions that are downright awesome!

Here are 3 key takeaways:

Upgrade Your Tools: If your accounting team is still relying on outdated methods and tools, it’s time to move on. A modern approach minimizes errors, saves time, and enhances efficiency.

Demand Clarity: You deserve clear, jargon-free communication from your accounting team. Understanding your financials is key to making informed decisions with confidence.

Be Proactive: A great accounting team should anticipate challenges and opportunities, not just react to them. Proactive planning and strategic advice will keep your business ahead of the curve.

New Economy Team Members are Experts in Accounting for Entrepreneurs

https://neweconomycpa.com/wp-content/uploads/2024/08/340.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-08-23 17:44:552024-08-23 17:46:18Reasons Your Current Accounting Team Sucks

But sometimes the accounting side of things can feel like a never-ending game of Whac-A-Mole.

And some days, you’re not the one doing the whacking, you’re the mole getting hit over the head.

Ouch.

We feel your pain.

Or, we used to.

And that’s why we love our work here at New Economy.

We love helping our clients reduce their financial pains so they can focus on greener pastures, hopefully not nearly as mole-infested.

Your accounting team has a tough job, but the end goal is to reduce your pain, not make more of it. So, let’s share some ways your accounting team is (hopefully) working to make your life better right now.

1. The Pain of Inefficiency and Wasted Time

There’s a reason for computers and AI, and it’s not to steal our jobs.

It’s to take on the work that would be otherwise boring, repetitive, or inefficient for a human to spend their brain power and time focusing on.

The software exists for most of these tasks, from bank reconciliations to expense tracking. It just needs to be well-implemented.

Your accounting team can help you out with the following:

Automate Repetitive Tasks: From invoicing to expense tracking, automation tools can handle the mundane so your team can focus on more exciting stuff. Less grunt work, more strategic thinking!

Optimize Workflows: Implementing streamlined processes reduces the time spent on repetitive tasks, freeing up resources for more important activities.

Improved Morale: Have you ever worked at an inefficient place that was constantly putting out fires? Compare it to somewhere that knew what was going on, had processes in place, and treated you like the intelligent person you are. Letting your employees plug into the processes, and then freeing up their minds to find innovative solutions is a great way your accounting team can help.

2. The Pain of Accounting Errors

We all make mistakes, it’s part of being human.

But how many times have your finances been thrown off by a tiny bookkeeping or accounting error?

Whether it was you or someone on the accounting team, someone spent hours, maybe even days, combing through the transactions and calculations to figure out what went wrong.

It’s a much better learning process to make interesting mistakes – like rethinking your marketing or investment strategies – compared to dealing with manual data entry errors.

And unfortunately, financial errors are more than just a headache—they can be expensive.

Here’s how your accounting team can help you avoid these pitfalls:

Implement Checks and Balances: Regular reviews and reconciliations catch errors before they become expensive problems.

Use Error-Prevention Tools: Some accounting software can identify potential errors before they impact your bottom line, or eliminate them by the automation we spoke about earlier.

Invest in Training: Ensure your team is well-trained to handle – and prevent – financial task errors.

3. The Pain of Taxes

We love the benefits taxes bring to our society, but we don’t love overpaying more than our fair share.

By optimizing your tax strategy, accountants help ensure you’re paying what you owe—nothing more, nothing less.

Strategic Tax Planning: Planning your tax strategy throughout the year avoids last-minute scramble and headaches. We know they’re coming – there’s no need to add extra stress just because it’s tax time!

Stay Compliant: Avoid penalties by ensuring you meet all your tax obligations correctly and on time.

Leverage Deductions and Credits: Your accountant can spot deductions and credits you might miss, ensuring you get the maximum benefit.

4. The Pain of Audits

Whether it’s an internal audit to ensure everything is in good shape or a visit from the IRS, audits strike fear into the hearts of business people around the world.

But they don’t have to be nightmares.

Your accounting team can simplify the process to make audits smoother and less stressful, with steps such as these:

Organize Documentation: Keeping your records neat and accessible to make the audit process a breeze.

Prepare in Advance: Regularly reviewing and preparing your documents so you’re not caught off guard during an audit.

Working Collaboratively: While your accounting team can handle the heavy lifting of audits, the sooner you can get info to them, the easier the jobs will be for everyone. While you don’t need to be an accountant, feel free to ask questions and learn the basics, because at the end of the day, you need to understand what’s going on financially in your business.

5. The Pain of Overwhelm and Second Guessing Your Strategy

It’s easy to be overwhelmed with the decisions you make for your business. Adding a bunch of numbers and financial reports on top of that may make things even worse if you’re not someone who feels comfortable with the financial side of running a business.

No one makes perfect decisions, but if you’re confident your numbers are accurate, and you have the correct reports, you can ask the right questions and make solid decisions.

A skilled finance and accounting team can offer expert advice and enhance financial reporting to ensure you’re not flying solo.

With their support, you’ll make informed decisions and feel more confident in your financial strategy.

They can help you by:

Clarifying Financial Reports: Make sense of your financial statements with expert advice that turns complex data into understandable insights.

Providing Strategic Insights: Receive guidance on making strategic decisions that align with your business goals, including tools such as business scorecards.

Putting Together a Scorecard: Your business scorecard can be an invaluable tool.

Supporting Big Decisions: Whether it’s expansion or cost-cutting, your accountant can provide insights and expert perspectives on the financial side to ease the process.

Preparing for Funding Opportunities: Whether it’s investments or bank loans.

3 Key Takeaways

At New Economy, we help you use financials to make more money and better business decisions so you’ll feel less pain when running your business. Those poor moles need a break as much as you do!

Streamline Your Processes (and Minimize Errors). Get rid of those repetitive tasks and reduce financial slip-ups by automating processes and leveraging efficient tools. A well-oiled accounting machine means fewer mistakes and more time to focus on what truly matters.

Simplify Audits and Tax Strategies. By keeping your records organized and planning your taxes smartly, you’ll make these daunting tasks much more manageable. Let your accounting team take the stress out of compliance and optimization.

Feel More Confident in Your Decisions. With clear financial reports and expert advice, you’ll be equipped to make informed decisions without second-guessing. Confidence in your financial strategy means less stress and more focus on growing your business.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/08/New-Economy.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-08-15 12:35:212024-08-15 12:36:14Top Ways Your Accounting Team Can Reduce Your Pain

We successfully graduated from a full implementation of EOS with a hired implementer back in 2020. The system has been instrumental in allowing us to build our team, systems and processes, and create company alignment around mission, vision, and values. It’s also helped us support our 3.5x revenue growth since implementation.

So clearly, we see the value in the EOS system.

Further, we greatly appreciate the EOS community’s shared values which encompass an abundance and growth mindset, doing the right thing, giving before you get, and doing what you say.

We are grateful to be a part of the community and want to help others just as we have been helped.

We have unique abilities in the data component that can be leveraged to help EOS companies achieve their vision and goals.

We want to help you gain control of your finances to make smart decisions to build and grow your company.

In this article, you will learn about:

Why to consider hiring a remote accountant and what to look for

The proper seats and core functions to set you up for success

The right tools and meeting rhythms

3 key takeaways

Let’s dive in.

What to Look for When Hiring a Remote Accountant and Why to Consider it as an Option

What to look for

New Economy is a fully remote Company. We have 15 team members in 15 different states. Further, we have 45 recurring customers that get us into another 5 states, totaling 20 states between employees and customers.

So we know firsthand that remote working works. We have leveraged the EOS tools and meeting rhythms which increase the probability of success.

We focus on:

Lots and of Leading, Managing, Accountability (LMA)

Focused and consistent Level 10’s, monthly check in’s, 90-day check-ins, Quarterly and annual roll-outs

Focused and consistent weekly, monthly and quarterly scorecards

Documented process

Technology to support the team and customers

Further, we outsource our marketing (awesome plug for Full Stadium 🙂) and legal (awesome plug for Howell Legal 🙂) to remote Companies. So not only are we a remote and outsourced service provider but we successfully leverage the service of others

So here is tip #1 – Make sure the company has proven experience and examples of success when working in a remote environment.

Many companies are trying to take advantage of remote working but they have not invested in the technology, process, or systems. They just are not equipped to provide awesome service (core value call out).

Another key component is alignment. Being an EOS company, we have a set of core values:

Deliver awesome customer service

Embrace learning and growth

Be passionate and own it

Build open and honest relationships

Continuous learning and growth

And we even look at our core values and seek to find alignment with our customers by asking questions during the early stages of the customer journey. Further, by leveraging our core values we have created the characteristics of our ideal customer:

Mission-driven, values-based, and growth-minded

Revenues and/or investor funding in excess of $2M

10+ Employees

Located anywhere in the US

Leverages technology and process

Wants an engaged accounting and finance partner to help them use data to grow

If this is you, let’s talk.

This leads to tip #2 – Make sure there is a degree of alignment around core values, working and communication styles.

This takes a bit of hard work, but as an EOS company, we know it’s all about getting the right people in the right seats, and the right person just might be someone that is remote.

So now we have a sense of what to look for.

But why should I consider outsourcing to a remote company?

Why to consider outsourcing

Back in June we wrote a detailed blog posting giving 3 key reasons why you should consider outsourcing to a remote accountant. For your reading pleasure, we are including a link here.

But if you like summaries, here are the top 3 reasons why:

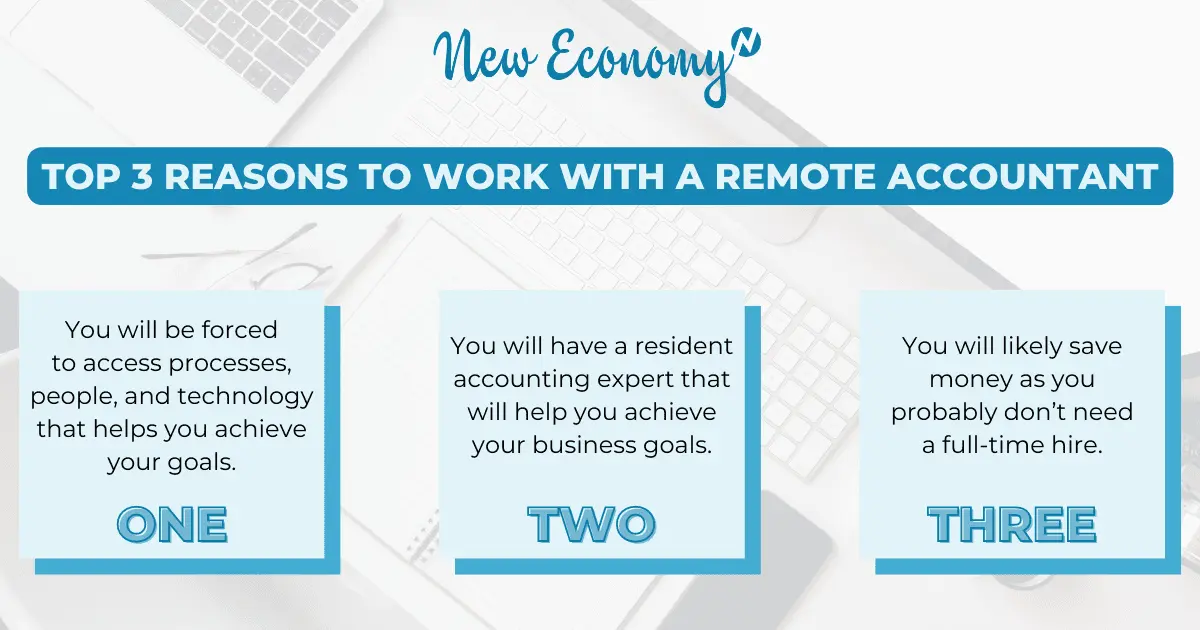

You will likely save money as you probably don’t need a full-time hire. You won’t need to worry about space, technology, or benefits. Further, you will not be overpaying a technical person to do admin-type work. We stay in our lane and focus on what we are good at which aligns with the seats and core functions which we will talk about later.

Considering outsourcing will require you to focus and evaluate your accountability chart, your people, your processes, and your technology. And this is a good thing for your business. It will require you to take a hard look at what is working, not working, and why. And one of the things about remote working and leveraging technology and process is effectiveness and efficiency because we have to.

You will have a resident accounting expert on your team who does not need to be trained or managed. They work with different companies so have an inside look into many businesses and acquire best practices. They are focused and specialized in core functions that are specific to their skill set.

So, by now you should have a sense of what to look for and why to consider outsourcing to a remote accountant.

Keep reading if you want to get a glimpse of seats and core functions in the accountability chart that will help you gain control of your finances to make smart decisions to build and grow your business.

The Proper Seats and Core Functions to Set You Up for Success

ou are probably familiar with the accountability chart if you run on EOS, and if not check out this quick video here. It acts like an organizational chart by really focusing on identifying the core functions of each role.

This is all about getting the right people in the right seats and focusing on accountability for the tasks they are responsible for.

We figured the best way to explain the ideal chart for a growth-minded organization is to just show it.

We prefer to build this from the bottom up:

First up is your staff accountant. This team member is leveraging processes and technology to perform their core functions. They are the foundation of your accounting team. The old saying is garbage in, garbage out. The tactical inputs of this team member will be at the front end of the strategic outputs you are looking for.

Staff/Senior Accountant

*AR and AP

*Payroll

*Bank & Credit Card recs

*Maintain QB

Next up is your Controller. This team member leads and manages the staff or senior accountant. Further, they work with creating processes and policies, and are focused on delivering timely and accurate financial information.

Controller

*Lead, Manage, Accountability

*Month-end close

*Financial process

*Budgeting & cash flow

Next up is your CFO. This team member sits on your leadership team. They are focused on being the right hand to the CEO and supporting the overall strategy of the business.

CFO

*Leadership

*Strategy

*Capital raising

*Risk

The above 3 seats are key for really every business, but it’s hard for a CFO to be effective if the foundational pieces are not in place. Remember, each role requires unique abilities and skills, so make sure you are setting everyone up for success.

Here is what a health accountability chart for a growth-minded company should look like:

CFO

*Leadership

*Strategy

*Capital raising

*Risk

Controller

*Lead, Manage, Accountability

*Month end close

*Financial process

*Budgeting & cash flow

Staff/Senior Accountant

*AR and AP

*Payroll

*Bank & Credit Card recs

*Maintain QB

For more information on the difference between an accountant, controller and CFO, check out this blog posting here.

And here are a few pro tips:

Tip #1 – Start from the ground up. Get the tactical foundational stuff set up before bringing in a controller or CFO.

Tip #2 – Don’t over-hire. Meaning, your CFO or Controller should not be doing admin-type work. Actually, they should not be doing any work outside of the core functions listed above.

Tip #3 – The reality of it is outsourcing can save you money. Focus on the core functions which are based on specialized skills. Use Admin and operations people for all non-accountant and finance core functions.

If you are feeling pain in this area, let’s talk. We have this figured out for you so you can focus on building and growing your Company.

The Right Tools and Meeting Rhythms

Now let’s talk about tools and meeting rhythms.

The Tools

Being a fully remote company, we operate in a paperless environment with all web-based applications. There are hundreds of web-based platforms out there to meet your needs and we don’t have time to go over all of them here, but here are some essentials:

Quickbooks Online – Maintains all of your accounting and produces your financial statements

Bill.com – Provides bill payment solutions that automate and help with internal controls

Expensify – Provides expense reimbursement solutions that automate and help with internal controls

Fathom – Provides month end dashboards and analysis like budget versus actual

Jirav – Provides budgeting and forecasting

And the list goes on. The key is to find a tool that is in the cloud and will add value to your life. The goal is to become more efficient as a result of the technology.

The Meeting Rhythms

Being remote, we live and die based on accountability. One of the ways we drive accountability is by having preset meeting rhythms. Much of this depends on the services our customers want but here is a glimpse into the preset rhythms we have in place:

Internal

Weekly Team Level 10’s – Here we all get on the same page for what’s working, not working and solve problems

Monthly Team member one on one – Make sure our team members are set up for success and help them with challenges and issues

Quarterly Check-Ins – These are 90-day check-ins where we provide our team with feedback and actionable insights to help them grow.

Monthly Culture Events – These are geared to help us grow in our relationships with each other. We are looking to build intentional connections and increase trust and credibility.

The above meetings impact our clients even though they are not a part of them. These meetings help to build our team up and provide clarity on timing, expectations, and deliverables. Most importantly they set the tone for our culture which is an internal thing that makes its way into everything we do.

Now onto our client-facing meeting rhythms:

External

Weekly Check-ins – These are to drive alignment and build trust. They are quick meetings to “get on the same page”. Some happen in Slack and others in Zoom.

Weekly Cash Flow – If we are doing bill pay or cash flow forecasting, we have a weekly cash flow meeting. This is to provide insights into cash flow on a rolling 13-week basis. (Read more about creating and following a cash flow model here).

Monthly Finance Zoom – This is a fun meeting and core to our services. Here we present the financials with actionable insights. We are quickly spoon-feeding our customers relevant information from the financials to make smart decisions.

Quarterly Tax Zoom – If we are providing tax consulting services, we connect quarterly to discuss tax opportunities and threats with the idea of providing peace of mind around taxes.

Quarterly Budgeting Zoom – If we are providing budgeting or forecasting services we will meet quarterly to discuss what we have learned about the business and how to apply it moving forward.

Ok, that seems like a lot and there is more. Note, that we love to simplify and can combine and condense where it makes sense.

The key for us is to have preset meetings that drive engagement. This engagement allows us to provide key insights to help our customers grow their businesses.

Here are three key takeaways:

You made it this far, now for the top 3 takeaways:

Spend time reviewing your business needs as they relate to your accounting department. What’s working or not working? Get this all documented based on the above accountability chart. Once you have established the seats and functions you can then move on to getting the right people involved.

Don’t overpay or underutilize team members. Meaning, your CFO should not be in QuickBooks doing basic accounting work. Further, your accountant should probably not be advising you on strategic business decisions. Build some depth on your team and outsourcing will provide a cost-effective way to make that happen.

Culture. Culture. Culture. We love to focus on alignment. Make sure you take the time to align with a company that seems to have a shared value system. Ask them about their mission, vision, and values and look for areas that resonate with you. Taking your time to get the right people in place will provide tremendous value in helping you achieve your goals and allow you to focus on what’s most important.

New Economy Team Members are Experts in Accounting for Entrepreneurs

If you run on EOS and building out processes with a focus on accountability is something your business is working towards, New Economy can help. We have the right tools and meeting rhythms to ensure your core functions are being taken care of.

Again, it’s our goal to help you gain control of your finances to make smart decisions to build and grow your company.

https://neweconomycpa.com/wp-content/uploads/2023/11/192.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2023-11-01 15:55:502023-11-01 15:57:50Why Companies Running on EOS Need a Remote Accountant in their Accountability Chart

How Leveraging Financial Data and Your Accounting Team Can Help.

As a growth-stage entrepreneur, you’re constantly dealing with emotional highs and lows based on the various circumstances thrown your way that are not in your control.

We feel your pain.

And we have learned that this can impact the confidence you have in your small business. But what really is confidence?

Here are a few definitions.

It is the feeling or belief that one can rely on someone or something.

Or defined another way, a feeling of self-assurance arising from one’s appreciation of one’s own abilities or qualities.

Or the state of feeling certain about the truth of something.

Which begs the question: Do you have confidence in your small business? And can you increase that confidence in your small business using financial data and leveraging your accounting team?

At New Economy, we believe so.

Why, you ask?

It aligns with our efforts of helping you gain control of your finances to make smart decisions to build and grow your company.

In this article, you will learn:

What types of issues might be eroding your confidence in your small business

What you can do to overcome these issues

Three key takeaways related to improving the confidence in your small business using data

Let’s dive in.

What Issues May be Eroding Your Confidence in Your Small Business?

There are a few important things to discuss here.

First off, there is no silver bullet and the game of business covers a lot of ground. Therefore, we will focus on issues on the financial side of your business, which is the space that we play in. But this approach can be applied to any department such as marketing or even operations.

So what could deteriorate your confidence in your small business as it relates to the financial side of your business?

Maybe it’s people, maybe it’s process, maybe it’s technology, or maybe it’s a combination of all three.

Let’s Talk People

Start with the Right Seats

Before we dive in, let’s discuss the seats in your accountability chart. And here is a question–Do you have a sense of the right seats and core functions needed for your business based on your stage, growth trajectory, and goals?

Bookkeeper / Accountant– They focus on tactical things like payroll, bill payment, bank reconciliation, credit card reconciliations, and invoicing and collections. This team member may have 3-5 years of experience.

Controller – They focus more on the output which would be things like accurate financial statements, accounting processes, managing the Bookkeeper, and working directly with the CEO or CFO. This team member may have 10-15 years of experience.

CFO – They focus on the business. They are a strategy partner to the CEO and they oversee everything related to accounting and finance and will get involved in budgeting, forecasting, and helping to bring plans to life. This team member may have 20+ years of experience.

Now that we have the right seats in place, you need to find the right team members and this is where people come into the picture.

Then Find the Right People to Fill Those Seats

At New Economy, we ask ourselves a few questions about placing a team member in a seat such as the ones mentioned above.

First, are they aligned with our core values at New Economy? If not, they will not be a good fit for our company, and we don’t place them. If yes, we move on to the next question.

Do they get it, want it, and have the capacity to complete the functions needed for the seat? If not, they will not be a good fit for the seat and we move on. But maybe through training and development, we can get them there. And if yes, then we place them in the seat.

So, if you don’t have the right seats, or maybe you have the right seats but the wrong person in them, you will face challenges. Chances are:

You are frustrated

your team member is frustrated and feeling burned out

You are not getting financial information to make smart decisions to build and grow your business

So your confidence could be down to not having the right structure and seats in your accountability chart or not having the right people sitting in those seats.

Consider stopping doing your own bookkeeping or using Tom’s uncle’s cousin who really is a party planner! Take the time to get this right.

If you get this right, you will have an accounting and finance department that is aligned with your vision and provides useful financial data, actionable insights, and business improvements all to help you build and grow your business. This is an investment in your business that will return extraordinary results.

Let’s Talk Process

The next issue that might be eroding your confidence in your small business is the lack of process. At New Economy we are consistently reviewing our core processes, documenting them, and training others to ensure they are followed by all.

By having documented processes in your accounting and finance department you are ensuring that team members are clear on how to do things and you are mitigating the chances for errors, inefficiencies, or even fraud. Yup, we said fraud which nobody thinks about until it’s too late.

But here is the real reason the documented process is important: It will ensure that over and over again you have a procedure in place to consistently produce a desired outcome in a timely and accurate manner.

For example:

Processes will support the release of timely and accurate financial statements. A process around the month’s end will allow any controller to step in and provide you with financial data that you can rely on to make great business decisions.

Processes will ensure that bills are paid on time for goods and services that we have received (we have seen vendors getting paid for things they should not) and that payments are going out at the right amount per the actual purchase order and invoice.

Processes will ensure that your business is on track to meet its annual budget. At month’s end, the actual financials can be compared to the budget to show what is on and off track. From there, you can forecast the future based on what you are learning to see how you are lining up compared to the budget.

We prefer to rely heavily on processes. The process runs the business and the people step in to run the process. This takes time and effort but it is worth addressing in all departments in your company.

So, if your accounting team is always late with providing information, missing key information, or off on the accuracy we can see why your confidence might be down. And it may be due to a lack of processes needed to support where the business is currently at today.

A few final thoughts:

Having a documented process may not be enough. We believe that team members need to be trained in processes. Further, the process needs to be followed by all. So, you need a process to ensure that processes are being followed – yikes!

But in the end, the process will give you the confidence that you are receiving financial information that is both timely and accurate. And this will give you insights as to how your business is performing.

Let’s Talk Technology

Remember the old days when you used to get a set of financial statements printed on ledger paper?

We don’t! And if someone handed us a set of financial statements on ledger paper our confidence would certainly drop. We’d question, in a healthy way, if we could rely on the numbers.

See, we have built New Economy from the ground up by leveraging a technology stack that allows us to provide virtual accounting and finance services worldwide. It’s faster, more efficient, more cost-effective, easier to build processes, and easier to train team members on how to use technology tools.

However, many companies’ accounting and finance departments are still struggling to adopt new technologies that will increase efficiencies, reduce errors, and allow team members to spend more time analyzing information and providing actionable insights.

The point is: Consider what technology you might be able to use to change the game and build your confidence.

But the main point is that the use of technology can speed the flow of information up and assist with increasing the accuracy. Further, processes can be wrapped around these technology tools, meaning technology has an impact on increasing your confidence in your small business.

What Can We Do to Overcome the Issues that are Decreasing Your Confidence in Your Small Business?

The very first thing we suggest you do is step away from the day-to-day of the business. Most growth-stage entrepreneurs have too much on their plate and it’s hard to reflect and think strategically when you are in the business.

So what do you do?

Take clarity breaks. A clarity break is a regularly scheduled appointment on your calendar with yourself. You define what regular is – a half-hour daily, two hours weekly, a half-day monthly. It’s up to you. The doing of it is what matters.

Note: We like to take these in physical spaces that motivate, inspire, and encourage us. For example, I like to take my clarity breaks in my 1986 VW camper van by the ocean. Some team members like to take them at Starbucks. But the point is, get away from your regular space.

OK, so I am in my van, now what?

We would encourage you to reflect on the above and ask the following questions:

Do I have the right accounting and finance seats on my accountability chart?

Are the functions for each seat clearly defined?

Do I have the right team member with the right skills sitting in the seat?

Do I have processes supporting each function in these seats?

Are the processes being followed by all? Are they evolving with the business?

Do I have the right technology to increase productivity?

Reflecting and answering these questions will increase your confidence in your accounting and finance team and provide you with the information you need to build and grow your business such as:

Ways to increase profits

Ways to mitigate risks

Ways to run smoother

Ways to improve business insights

And ultimately increase business confidence

We have subscribed to this approach to help build and grow New Economy. You can do this for literally any department in your business.

But should you want to get there quickly, consider hiring a company like New Economy that has done the hard work for you 🙂

And once you have the confidence in the back end of your business, you are ready to go and ready to grow. You have the foundation built to support the needs of your customers while capturing market share.

3 Key Takeaways Related to Improving Confidence in Your Small Business Using Data and Leveraging Your Accounting Team

If you want to improve your confidence in your small business, consider leveraging your accounting and finance team and the data they provide.

Here are three key takeaways related to improving your small business confidence:

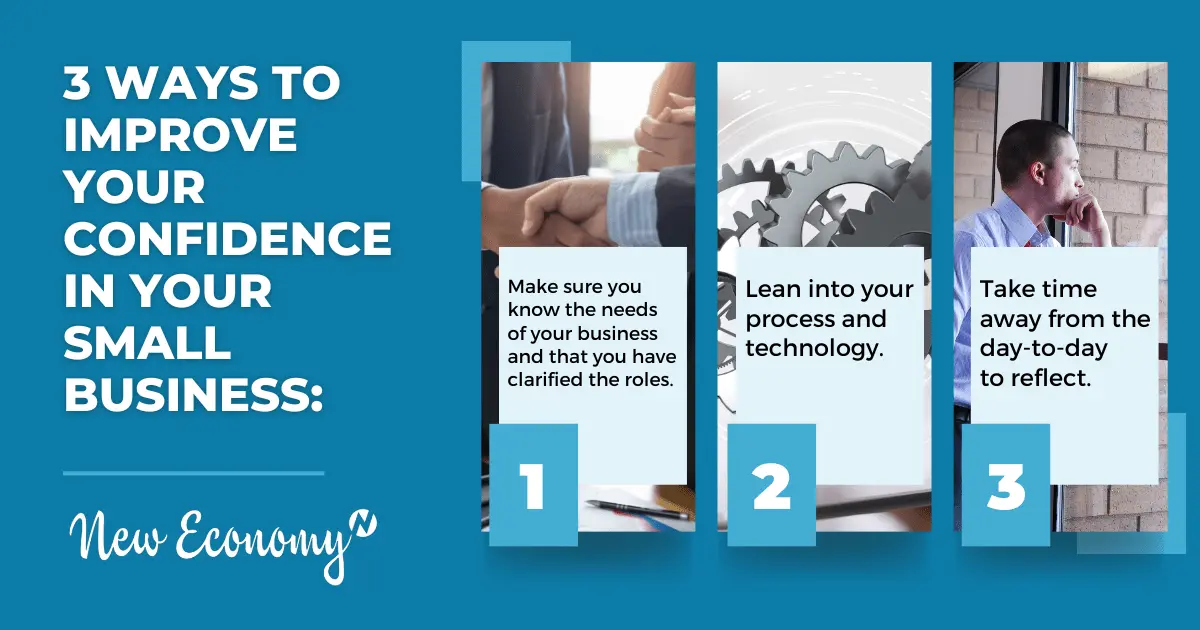

Make sure you know the needs of your business and that you have clarified the roles. Further, make sure that you have the right person with the right skill set to meet those needs by being able to perform the core functions of the role.

Lean into your process and technology. Make sure that you have a documented process followed by all. Further, make sure that you are using the best-in-class technology for efficiency purposes.

Take time away from the day-to-day to reflect. Think about what’s working and not working, and what next people move you need to make. This time is valuable in that it will provide new ideas and actionable insights to chase down your goals.

New Economy Team Members are Experts in Accounting for Entrepreneurs

If your Company’s accounting and finance team is not providing data to help build your confidence in your small business, let’s talk.

https://neweconomycpa.com/wp-content/uploads/2023/08/New-Economy-3-1.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2023-08-23 14:50:552023-08-23 16:35:163 Ways to Boost Your Confidence in Your Small Business

If you are an entrepreneur, your skill set is probably not in accounting. You are a visionary, a risk taker, you have guts, you have passion and you are trying to add value to the world by solving a problem.

But your accounting is important.

In this article, you will learn:

What is accounting for entrepreneurs and who does it?

Why accounting is important for entrepreneurs

What to expect as your business grows

3 key takeaways related to accounting for entrepreneurs

Let’s dive in.

What is Accounting for Entrepreneurs and Who Does it?

Accounting is the process of recording financial transactions pertaining to a business. The accounting process includes summarizing, analyzing, and reporting these transactions to:

Oversight agencies

Regulators

Investors

Leadership teams

Tax collection entities

We encourage all entrepreneurs to engage in the process of accounting from day one. But the extent depends on the needs of the business and it evolves over time.

Many entrepreneurs that have under $1,000,000 in raised capital or revenue will take the “do it yourself” approach. But Entrepreneurial companies with over $1,000,000 in raised capital or revenue will seek the support of a remote outsourced accountant.

Accounting takes work. There is a setting up of an accounting platform like QuickBooks online. Setting up bank feeds into the platform. Categorizing transactions. Completing all the detailed reconciliations. Creating and executing accounting policies. Yes, we can automate and use A.I. but it still takes work.

The accounting is done with the purpose to produce timely and accurate financial statements to provide you with financial information to make smart decisions to build and grow your business.

Why is Accounting for Entrepreneurs Important?

There are a few different reasons why accounting for entrepreneurs is important.

But most importantly, the accounting will result in having financial statements that will help you access the financial condition of your business. You will be able to use it to ensure you are on track to achieve your goals.

Here are a few other reasons why accounting for entrepreneurs is important:

IRS – You are going to be required to file an accurate tax return for your business at the end of the year. The accounting that is done will allow you to efficiently and effectively file this tax return with the IRS and keep you out of jail 🙂

Inventors or Banks – By engaging in the process of accounting you will be able to provide financial information your investors will be asking for, like financial statements to determine the financial health of your business.

Leadership Teams or Decision makers – These folks are responsible for ensuring the strategic plan is on track and making business decisions. By producing a monthly financial statement from your accounting process, this team will be able to evaluate if the business is on or off track with its financial plan and overall business strategy. If there is no leadership team in place, this information is still very useful to the CEO or business owner. The idea is to use the data to make smart decisions and not just go off your “gut” or how much cash you have in the bank. This is probably the most important reason to engage in accounting for your entrepreneurial business.

What to Expect as the Business Grows?

As your business grows things will get a bit more complicated and your systems process and team will need to evolve.

Initially, your accounting team might just need an accountant. This team member will be focused on more tactical things like running payroll, paying your bills, invoicing your customers, and maintaining your Quickbooks Online.

When your business grows, you are going to need more timely and accurate financial statements. These financials will help you to make smart business decisions. This team member that will be working with you on understanding your financial results is a Controller. They are also responsible for setting processes and policies that will evolve as your business grows.

As your business keeps growing it may require additional funding from an investor or bank. At this point in time, you might need a Chief Financial Officer (CFO). They are the right hand to the CEO or business owner and thinking about the future of the business and helping to provide future visibility in the form of a budget or projection.

At New Economy, we provide a little bit of each to our clients. Since we work with growing Entrepreneurial companies, there is a need for both tactical and strategic support to help the business achieve its goals.

As for Technology, much of it is scalable.

In our experience, there is some relatively inexpensive technology that is supporting businesses doing $5-$10M in revenue or in fundraising.

Here is a bit of the technology stack that we use at New Economy:

There is lots of technology out there and a remote accounting firm like New Economy can help you to determine the right fit for your business.

3 Key Takeaways Related to Accounting for Entrepreneurs

Being an entrepreneur is hard enough. You don’t need to worry about your accounting. You should be focused on building your Company and let us help you gain control of your finances to make smart business decisions.

Here are three key takeaways related to accounting for entrepreneurs:

No matter where you are in the business lifecycle make sure you have a certain level of accounting in place. If you are under $1M in revenue or funding it might be “DIY”. If it is more consider outsourcing your accounting to a remote accountant.

Continue to assess the accounting team you have in place. As your business grows, you should be increasing the depth of your accounting team to go from tactical support to more strategic support.

Leverage your accounting to help you achieve your goals. Your accounting will produce financial statements that will tell you if you are on track to meet your business goals. Use them well to make smart business decisions.

New Economy Team Members are Experts in Accounting for Entrepreneurs

Getting your accounting done and done right is the key to financial peace of mind for you and your business. That’s why our team at New Economy is an excellent partner.

We help entrepreneurs gain control of their finances to make smart decisions to build and grow their business.

https://neweconomycpa.com/wp-content/uploads/2023/06/New-Economy-1.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2023-06-14 12:21:282023-06-19 13:05:11Accounting for Entrepreneurs: What to Expect?

Outsourcing your accounting to a remote accountant could have some significant upsides to your business.

First off you are going to get an expert. That’s right you get the expert who will elevate your visibility by giving you new insight into the data side of your business.

But why is this important? The accounting expert can help you to assure that you are meeting your business goals by leveraging timely and accurate financial information. You will move from frustration and chaos around the numbers to clarity and visibility which will help you make smart business decisions.

In addition to adding an expert to your team, you can save money and have one less person to manage as newer web-based technology is enabling remote accountants to work with businesses entirely virtually and like never before.

Outsourcing to a Remote Accountant Looks Different for Everyone

Outsourcing to a remote accountant looks different from business to business based on what you need.

Do you need a tactical team member like a bookkeeper? They will handle day-to-day things like paying your bills leveraging software like bill.com.

Do you need a more strategic partner like a controller? They will deliver a timely and accurate set of financials to use to make smart decisions to build and grow your business.

We suggest referring to the accountability chart, otherwise known as an organizational chart, and understanding the role you are looking to place. Along with the role, you’ll have a better understanding of the core functions that will be outsourced.

For example, outsourcing a bookkeeper could include outsourcing functions related to:

Payroll

Bill payment

Invoicing and collections

Bank reconciliations

Once you land on the role, then it’s a matter of process. Going back to the example of the bookkeeper and specifically bill payment, you need sound processes and clear expectations.

For example:

Pay bills every two weeks by the bookkeeper

Ensure all POs are matched to invoices and shipping documents by operations

Obtain proper approval for the release of the payment by operations

Release payment by the bookkeeper

Note: All of these processes can be executed by leveraging inexpensive but highly effective software.

The last key piece is having a culture and environment that enables and leverages technology. If you have the right person and the right process this is the final piece.

Back to our bill pay example, we leverage a piece of software called bill.com. It enables us to create and execute against the process we laid out. For instance, there are approval features and you have the ability to upload the relevant documents needed for approval into the system, allowing the approver to have access to them when approving.

Watch this to hear from our Founder on the 3 reasons to outsource your accounting to a remote accountant:

Does Outsourcing Make Sense for You?

If all of your technology is housed in a closet in a server room then outsourcing to a remote accountant might be tough, as it’s an important piece to making this work.

On the other hand, if you are leveraging web-based platforms like QuickBooks Online, Bill.com, Gusto, and Drop Box you are on the right track to creating a technology stack that can be used.

Fear not, if you have the desire to transition into the digital world that is an option too.

Here is a question for you:

What are the qualifications of the person maintaining your books, financials, and projections?

Many companies have a person in the accounting or bookkeeping seat that is not qualified.

Basically, they got the short end of the stick! But imagine a world where you had access to a team member that had unique abilities in this area as a trained professional. They are efficient, effective and provide relevant financial information to help you make smart decisions to build and grow your business.

That’s what we are really talking about. A team of experts that will be operating as a partner to provide data to help you make good decisions.

Lastly, there can be significant cost savings to outsourcing to a remote accountant. The key to this is to have this person focus on core functions that relate to their specific technical skills. You don’t want your accountant getting into HR or administration. You want them to focus on specific tasks that require their knowledge.

Top 3 Reasons to Work with a Remote Accountant

1/ Moving into this arrangement will force the business to access processes, people, and technology to ensure that you have efficient and effective people, technology, and processes to help you achieve your goals.

2/ You will have a resident accounting expert that does not need to be trained or managed. They will help gain control of your finances so you can build and grow your business.

3/ You will likely save money as you probably don’t need a full-time hire. You won’t need to worry about space, technology, or benefits.

Searching for a Remote Accountant?

If you’re looking to outsource your accounting to a remote accountant – look no further.

New Economy exists to help entrepreneurs gain control of their finances to make smart decisions to build and grow their business.

https://neweconomycpa.com/wp-content/uploads/2023/06/New-Economy.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2023-06-08 12:02:562023-06-14 12:14:163 Reasons to Outsource Your Accounting to a Remote Accountant

To help you understand how to create and follow a cash forecasting model, let us paint a picture for you.

The Hero

Every hero has a story. And we are big fans of the hero. You are the hero in this story.

Picture yourself as Luke Skywalker.

You are the entrepreneur working really hard and doing amazing things. You have guts, passion, and are willing to put it all on the line. We understand where you are coming from and have tremendous respect for you.

But we also understand that it’s not easy.

The Problem

In every story, the hero has a problem to solve. Some are more challenging than others, there is a problem we see over and over again.

Entrepreneurs:

Don’t have the financial visibility to know when cash needs will arise

Don’t know how to be proactive to avoid these needs

Don’t have the time to pull the information together

Don’t have the unique abilities to work through the issues

This is your Darth Vader and it can have massive implications on your ability to build and grow your business. Nobody wants to run out of cash.

The Guide

Another essential aspect of a good story is a guide.

New Economy, with its team of experts, financial tools, and trusted processes, is grateful to play the role of the guide.

We want to help you solve the problem. We want to help you succeed. We are your Yoda.

In this article, we’ll take the opportunity to explain how we can help you solve this common problem i.e. get rid of your Darth Vader. Specifically, we’ll talk about the importance of visibility around cash flow and the projection tool we use to help our heroes become triumphant.

The Cash Forecasting Model aka The Tool

Here at New Economy, we believe that entrepreneurs need a tool to see their cash flows out into the future. We like to provide this visibility over a rolling 13-week period.

Our tool is very easy to use and is accessible by way of Google Sheets.

It’s our goal to start simple and solve the problem at hand (lack of data for visibility and decision-making), only then will we introduce automated technology and dig deeper into your finances.

Before diving head-first into your cash forecasting model, you need to do some planning, investigating, and info-gathering.

This can be a time-consuming process, so be patient and give it the time it needs, ensuring your records are thorough and complete. Keep in mind, hard work now has the possibility to make massive impacts on your business and help you sleep better at night :).

Here are some simple steps you can take to get started:

Analyze historical spending

Understand spending needs

Cut, reduce, and extend payments

Identify cash flow gaps

Identify solutions to cash flow gaps

As you gather this information, you’ll need to get deep into the “weeds”. Look at your accounts receivable and accounts payable journal and take a close look at historical bank statements since we are talking about cash. These are the source documents that will be utilized to build out the tool.

We always advise clients to be detail-oriented because the more information you include in the tool, the better your results will be.

The above data will be utilized to show the cash in and cash out needs of the business. We will be leveraging the historical results to predict the next 13 weeks.

A great start is to sign up for that cash flow tool noted above which will walk you step by step through the process of building out the tool.

Your Transformation

Nailing down a cash forecasting model comes with plenty of benefits. You’ll gain stronger business processes and intelligence around:

Cash collection acceleration techniques

Proven effective collection policies

Proven effective credit policies

Proven effective payment policies

Building cash reserves

Preparedness on meeting obligations before they occur

Remember when we said a well-built cash forecasting model will greatly impact your business and help you sleep at night?

We meant it.

Ending with Success

What does success look like in your story? If gaining financial security establishes itself as a success indicator for your business, our team at New Economy has you covered.

With our help, we’ll work to help you get the feeling of financial security based on the ability to predict cash flow needs.

You’ll be able to:

Know when, where, and how your cash flow needs will occur

Know the best resources for meeting cash flow needs (Debt, Equity, Factoring)

Prepare to meet those needs in advance

Set goals for building cash reserves

Set goals for paying down debt

Improve collection processes and techniques

Your success is important to us and as a recession looms, cash forecasting models need to play an even larger role in your financial management processes as they can prepare your business for what’s to come.

https://neweconomycpa.com/wp-content/uploads/2023/04/New-Economy-1.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2023-04-25 15:40:402023-05-23 14:48:31How to Create and Follow a Cash Forecasting Model

As a growing startup, your business will eventually need to implement several key processes to continue achieving your business goals.

These processes will improve efficiency and help you complete the actions or operations needed to achieve your desired result.

Here at New Economy, we focus our processes on data. This gives us the best results and positions us for success.

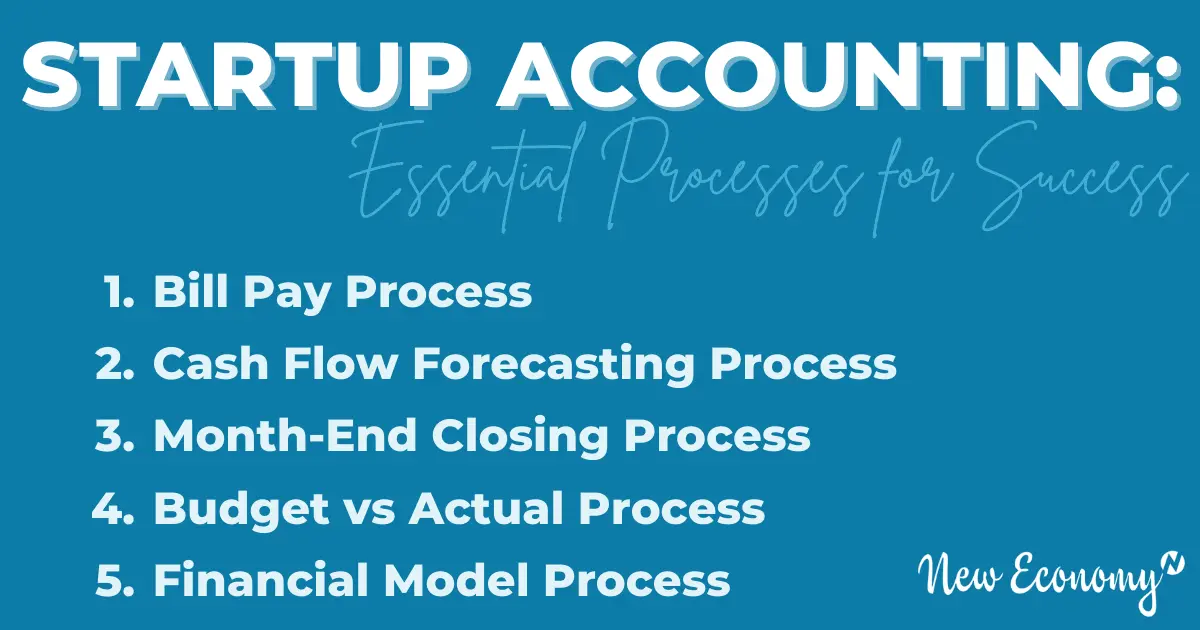

We have identified five essential processes that are handled by our team of accountants, controllers, and CFOs. This article will dive into these processes and explain how they work.

1. Bill Pay Process

Knowing how much cash (when and to whom it’s going) is leaving your business is important. This is where a bill paying process comes into play.

Here are some key steps for this process:

Establish a weekly rhythm to focus on this process. We like to use a schedule or calendar.

Ensure all documentation has been received such as invoices, shipping documents, and purchase orders.

Produce an accounts payable aging to show which amounts are due, to whom, and when.

Establish an approval process for payment ensuring that the goods or services have been actually received or provided.

Leverage technology to store digital documents and automate the approval process using technology like bill.com.

The bill pay processes are typically performed by staff or a senior accountant. The information is then leveled up into cash flow forecasting.

2. Cash Flow Forecasting Process

Attaching itself to the tactical bill pay process is a more strategic process in order to gain future visibility. Understanding your cash flow gaps is crucial to managing your business and achieving your goals.

Here are some key steps for this process:

Layer on extra time to your weekly bill pay meeting rhythm to get more strategic.

Load in all expected money due over the next 13 weeks and all money going out over the next 13 weeks. Then, verify the figure to your AR and AP aging.

Analyze and review for cash flow gaps.

Determine the next steps to cover the gap such as accelerating AR collections, leveraging a short-term loan, or extending terms on your accounts payable.

The cash flow forecasting process is a beauty. This process has helped many entrepreneurs sleep at night as it provides the visibility and data they need to make good decisions. This process is usually owned by a more experienced team member, like a controller.

3. Month-End Closing Process

All businesses need timely and accurate financial statements. Obtaining them each month allows you to determine how your business performed. This is beneficial as it will give you a snapshot of the financial condition of your business.

Here are some key steps for this process:

Set up an agreed-upon timeline to have the books closed. This is typically by the 15th of the month for the preceding month.

Prepare a month-end closing checklist. This includes things like complete bank reconciliations, credit card reconciliations, and ensuring revenue is properly recognized.

Complete the month end closing checklist to ensure that the accounting policies are followed. To ensure the books are accurate, accounting policies must be executed.

Book all adjusting entries that are necessary for accurate books.

The goal of the month-end closing process is to ensure that your numbers are accurate. This is important as you’ll need to leverage your month-end financials to build and grow your business. This process is usually owned by a more experienced team member, like a controller.

4. Budget vs Actual Process

Attaching to the month-end close process is the budget versus actual process. This process allows you to understand, line item by line item, how the business is performing against plan.

Produce a system-generated budget versus actual report.

Review variances and determine if the variance is a timing issue or a real business issue that needs to be addressed.

Share the variances with department heads or others that can be held accountable to influence change.

The goal of this process is to determine where the business is over or underperforming. This is great data to have as points you in the right direction and gives you the opportunity to ask yourself if things need to change. This process is usually owned by a more experienced team member, like a controller.

5. Financial Model Process

Building and maintaining a three-statement financial model by month, over the next 12-18 months, is crucial. It provides a picture of what the business looks like in the future and what resources are needed to bring that vision alive.

Here are some key steps to this process:

Gain an understanding of the overall business model and drivers.

Review relevant contracts and agreements that are pertinent to the business.

Build out a three-statement model being a balance sheet, income statement, and cash flow.

Adjust the model each month based on what you have learned about the business.

Iterate, iterate, iterate as this is a living and breathing document.

The goal of this process is to provide you with a flexible picture, based on your assumptions, of the future financial condition of the business. Further, it will provide you with a road map of where the business is headed. This process is usually owned by a more experienced team member, like a CFO.

Build Out These Processes for Success

With due diligence and the help of these processes, your business will be well-positioned for success.

If building out these processes sounds overwhelming or too time-consuming, reach out to New Economy. We help entrepreneurs gain control of their finances and make smart decisions.