Does My Business Need a Bookkeeper, Accountant, Controller, or CFO?

There’s a lot riding on your financial team, but how do you know if you have the right roles in place to maximize your success?

Are you asking your bookkeeper to drive your financial strategy?

Is your CFO wasting time on data entry?

Can’t I just hire an accountant and be done with it?

And what the heck is a controller?

Depending on the size and stage of your business, you may need some or all of these roles.

Making sure you have the right person for each job increases your efficiency and potential to knock your growth goals out of the ballpark.

But you may not need multiple full-time hires. Outsourced and fractional roles exist to assist growing organizations.

Before we get into that, let’s make sure we’re on the same page with every role and its functions.

What Does Everyone Do?

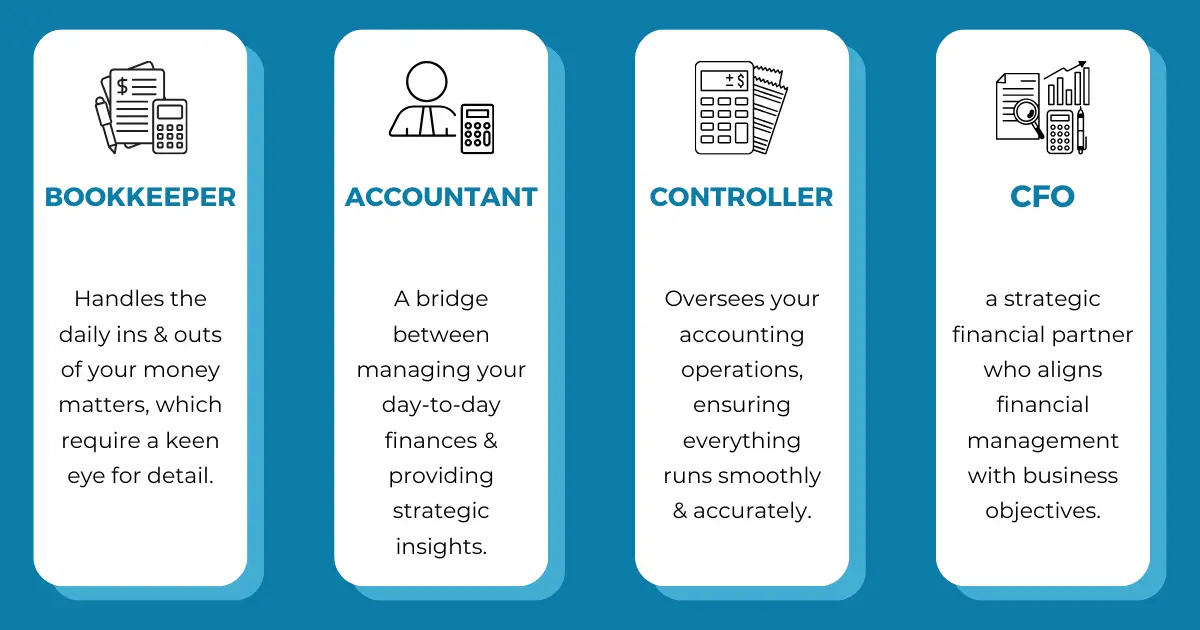

Bookkeeper

Bookkeepers handle the daily ins and outs of your money matters, which require a keen eye for detail. The time and energy to manage this work may weigh heavily on employees who don’t specialize in this, so a bookkeeper is often your first financial hire.

Key bookkeeper functions:

- Daily upkeep: Manages payroll, pays bills, and keeps your books in order.

- Keeps your financial house clean: Ensures all transactions are accurately recorded.

- First line of defense: Catches small issues before they become big problems.

Unlike accountants, who have the rigorous CPA designation to prove their expertise, bookkeepers do not have a standard designation. There are many bookkeeping certifications out there, and the quality varies, so it’s important to find someone trustworthy who has the correct training to do a good job for your business.

Accountant

An accountant is a bridge between managing your day-to-day finances and providing strategic insights. They particularly shine when it comes to helping you understand your financial statements and what they are telling you about the business. This is an essential part of any business, and a headache if you don’t have the right team supporting you.

Key accountant functions:

- Beyond bookkeeping: Prepares financial statements and ensures tax compliance.

- Insight provider: Delivers more in-depth reports and financial analysis.

- Tax pro: Helps you navigate the complex world of taxes, ensuring you pay what you owe and that you take advantage of the tax write-offs available.

Make sure you find an accountant with a current CPA designation if you’re going to be leaning on them in your business.

Controller

Controllers oversee your accounting operations, ensuring everything runs smoothly and accurately. They are pros at letting you know what has happened in the business based on the historical financial statements.

Key controller functions:

- Financial fidelity: Manages policies and internal controls to safeguard your assets.

- Team leader: Directs the accounting staff and integrates processes.

- Audit liaison: Prepares your business for external audits, ensuring compliance.

- Business Tools: Provide and support financial tools to run the business (i.e cash flow forecasting, budgeting).

While accountants and bookkeepers can also prepare for audits, controllers in particular excel in this area. They can help prevent audits by building strong controls, but when they are required, can ensure the process goes smoothly.

Chief Financial Officer (CFO)

Finally, we arrive at the CFO. Your strategic financial partner who aligns financial management with business objectives, especially during periods of rapid growth. They are the right hand to the CEO providing forward looking insights.

Key CFO functions:

- Visionary: Manages big-picture financial strategy, from capital raising to budget management.

- Growth navigator: Helps secure funding and manages investor relations.

- Strategic leader: Ensures the financial team supports broader business goals, maintaining budget discipline and strategic alignment.

How They Work Together

With so many moving parts, it may be hard to visualize how these roles work together in an accounting department. Let’s provide an example that is relevant for many medium-sized growing businesses.

The bookkeeper records daily transactions, ensuring that all financial data is up-to-date and accurately entered. This foundational work is crucial for accountants, who rely on these records to prepare detailed financial statements and conduct thorough tax planning. Some organizations may have several bookkeepers and accountants.

At the next level, the controller uses the reports prepared by the accountant to enforce and refine accounting policies and internal controls, ensuring that the financial operations run smoothly and comply with legal standards. This oversight helps to safeguard the company’s assets and improves overall efficiency, which is critical for the strategic work of the CFO.

With a well-managed financial framework in place, the CFO can focus on higher-level strategic planning and capital management. They can leverage the accurate and timely information provided by the controller to make informed decisions about investments, funding, and growth opportunities.

This strategic guidance, in turn, feeds back into the operational level, where improved processes and financial strategies help streamline everyday accounting tasks, creating a cohesive, supportive financial environment.

What Your Business Needs

While there’s never a one-size-fits-all solution, here are some general guidelines for when different roles make sense in an organization.

Small, Relatively Stable Businesses

If your business isn’t too big, and you’re not planning any major growth or changes, you’re probably fine with a bookkeeper and/or accountant. They’ll make sure your books are in order and compliant, and help prepare you for tax time. They can prepare financial reports to give you a sense of your business.

While your business may be small, it could make financial sense to have a bookkeeper and an accountant, even if they are part-time. Bookkeepers typically charge less, and you don’t need someone with a CPA doing extensive data entry. However, this approach only makes sense if there is good communication between all parties to avoid headaches.

Medium Businesses

If your business is medium-sized, a bit more complex but relatively stable, and you have many employees and streams of income… you might be at the stage where accountants aren’t quite enough.

In this case, you’ll want to consider adding a controller (even if only part-time) to your team. You wouldn’t want to risk the headaches and potential legal pitfalls of not having someone keeping a very close eye on everything going on in your business.

Startups, Rapidly Growing Businesses, and Large Enterprises

You may be ready for a CFO if your business is:

- Rapidly growing, regardless of size

- A startup that is looking to bring in more funding

- On the medium to larger size of the “Small to Medium Enterprise” definition

Managing finances with an eye for strategy needs sophisticated financial oversight. A CFO becomes essential to navigate capital increases, detailed budgeting, and complex financial forecasting when funding sources and growth are rapidly changing.

Fractional Roles

For many businesses, some or all of these roles can be part-time or fractional hires. This can allow a business to reap the benefits of the expertise of financial professionals, without the longer-term commitment and full-time paychecks.

For example, a full-time CFO can cost anywhere from $100-400K per year at an SME, if you’re including salary and benefits. However, an outsourced CFO could cost only $6-12K per month, depending on the services provided.

3 Key Takeaways

If you’re not sure how to build out your financial team based on your business size and stage, talk to our team at New Economy. We’re always happy to help!

Remember:

- Right Expertise, Right Time: Ensure you have the appropriate financial expertise at each stage of your business growth.

- Stay Proactive: Don’t wait for financial challenges to find you; have the right team in place and be ready for the future.

- Strategic Growth: Leverage the expertise of part-time and fractional financial team members who help rather than hinder your business success.

There you have it 🙂

New Economy Helps You Put Together Your Team

At New Economy, we understand that one size does not fit all when it comes to your financial needs. We’re able to help find part-time and fractional virtual support.

Whether you need a bookkeeper, accountant, controller, or CFO…we have the people who can help your finances thrive. We can save you time by ensuring you have vetted, professional finance experts to help with your business.

Schedule a time to meet with our Founder, Jeff, and discuss how our team can help your team thrive!