January flew by, and as we stepped into a new year, one theme kept surfacing: the power of intentional leadership.

Whether it’s embracing industry trends, navigating financial challenges, or inspiring a team, the best leaders don’t just react—they lead with purpose.

At New Economy, we believe that success starts with a clear vision and strong financial foundations.

This past month, we explored the key trends shaping 2025 and what it truly means to lead like you care.

Here’s what stood out to us and how these insights can help you build momentum for the months ahead.

Key Trends for Small Businesses in 2025

The business landscape is constantly evolving, and staying ahead means being adaptable.

In Newsletter #36 (sent on Jan 20), we highlighted an Entrepreneur article that outlined five major trends small business owners should watch.

Here are the most critical takeaways:

AI Integration: Leveraging artificial intelligence to streamline operations and enhance customer experiences.

Financial Resilience: Strengthening cash flow through smart financial strategies, including multi-currency accounts for international transactions.

Gen Z Influence: Aligning marketing strategies to meet the demand for authenticity, sustainability, and short-form content.

Sustainability as a Standard: Consumers increasingly expect eco-friendly practices, making sustainability a competitive advantage.

Adaptability in Uncertain Markets: Business owners who remain flexible will be best positioned to seize new opportunities.

For a deeper dive into these trends—especially financial resilience—check out the full Entrepreneur article here.

Leadership That Drives Real Impact

Trends and strategies mean little without the right leadership in place. Great leaders understand that their role goes beyond decision-making; it’s about creating a culture where people feel heard, valued, and empowered.

At the heart of strong leadership is one fundamental trait: care.

Caring leaders build trust, and trust leads to creativity, innovation, and long-term commitment. When leaders prioritize integrity, generosity, and a shared vision, they inspire loyalty—not just compliance.

True leadership isn’t about power or control; it’s about giving more than you take. When you invest in your team, you cultivate an environment where people thrive, push their limits, and contribute to something bigger than themselves.

If you’re looking for ways to refine your leadership approach, here are four great resources:

Great leadership and business trends won’t translate into success without financial clarity. Many businesses unknowingly operate with financial blind spots that can hinder growth.

That’s why we created a Financial Health Checkup.

This quick quiz helps you identify potential gaps in your financial strategy so you can make informed decisions and scale with confidence.

Our team is always working to provide valuable resources for business owners. Here are a couple of things to keep on your radar:

1. Referral Program: Help Others & Get Rewarded

We’re always looking to connect with ambitious entrepreneurs. If you refer someone to New Economy and they become a client, you’ll unlock exclusive benefits.

If you have any questions about our referral program or how to get connected with New Economy, feel free to reach out!

Key Takeaways As We Dive Deeper Into February

As we build momentum into the next month, here’s what we’re carrying forward:

Leadership is Rooted in Care: The best leaders foster trust, loyalty, and innovation.

Adaptability is Key: Understanding and embracing small business trends will set you up for success in 2025.

Financial Health Drives Growth: Identifying and addressing financial blind spots is crucial for long-term success.

There you have it 🙂

At New Economy, our passion is helping entrepreneurs gain control of their finances so they can make smart decisions and scale with confidence. Whether you’re leaning into new trends or shifting your leadership approach, we’ll be here every step of the way.

https://neweconomycpa.com/wp-content/uploads/2025/02/New-Economy-34.png6301200Mallory Raberhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngMallory Raber2025-02-13 11:22:242025-02-13 11:22:24In Case You Missed It: Leading with Purpose & Staying Ahead in 2025

The role of an EOS Integrator is critical for driving organizational success.

An Integrator acts as the glue that holds the company’s operational and strategic initiatives together, transforming the visionary’s ideas into concrete results.

The challenge for the integrator is, by nature, that you’re required to pull many disciplines together while wearing multiple hats.

How do you keep the company aligned on the vision?

How do you ensure accountability for sales goals?

Are meetings all happening on schedule?

In this post, we’ll explore some of the fundamentals of the role, and provide practice steps toward success.

The Role of an EOS Integrator

An Integrator must wear many hats: they are a fierce communicator, a unifier, and a problem-solver who ensures that the company’s vision is systematically executed.

To faithfully execute the business plan, Integrators must understand every crevice of the company, hold teams accountable, foster company-wide transparency, and ensure all oars are moving in unison.

There are telltale signs when an organization could benefit from a stronger Integrator:

A palpable lack of accountability

Persisting issues that resist resolution

Sluggish decision-making

An effective Integrator attacks these symptoms by drilling to the root of challenges, demanding action and follow-through, and facilitating speedy yet thoughtful decisions.

Where Good Accounting Fits In

Good accounting practice is not merely a matter of keeping books in check.

At New Economy CPA, we believe that it is foundational to the successful execution of EOS. A remote accountant in your accountability chart is essential.

But why?

Financial Clarity Leads to Accountability

Sign one of the need for a stronger Integrator, a deficiency in accountability, can be magnified when financial insights are blurry.

An Integrator armed with clear financial statements can:

Set realistic goals

Measure achievements accurately

Motivate teams with objective progress tracking

Remote accounting professionals provide real-time data and financial analysis that empower Integrators to hold every department accountable effectively.

This ensures not just achieving but exceeding those all-important quarterly rocks and scorecard numbers.

Uncover Issues with Precise Data

The second sign, recurring issues, often finds its genesis in misaligned or misinterpreted data.

When an Integrator collaborates with knowledgeable accountants, they gain access to meticulous financial reports that shed light on underlying problems.

Identifying, discussing, and solving – the EOS IDS process – benefits immensely from the insights that comprehensive financial information provides.

When financial trends and anomalies stand out, Integrators can guide their teams in resolving issues at their root, not just their symptoms.

Decision-Making Empowered by Real-Time Financial Insights

Slow decision-making, the third sign, could indicate a lack of immediate access to financial insights necessary for sound judgment calls.

The integration of remote accounting ensures that accurate, up-to-date financial data is readily available for quick, informed decision-making.

When an Integrator understands the fiscal implications of each choice, meetings transform from mundane to strategic, from a chore to a decisive action hub.

Thriving as an EOS Integrator with a Financial Perspective

To thrive as an EOS Integrator, it is imperative to foster the “Grow or Die” mindset with a robust grasp of organizational finance.

Here’s how an Integrator can amplify their impact through good accounting:

Establish Financial Scorecards: Work with your remote accountant to develop financial scorecards that are as critical as operational scorecards in gauging company health.

Financially Focused IDS: Engage in IDS sessions where financial insights drive the discussion, ensuring the company’s financial health is front and center.

Budget Adherence: Reinforce budget discipline across departments, showing the direct impact on company goals.

Drive Financial Growth: Set concrete financial targets and pair them with operational goals to synergize the teams’ efforts.

The best Integrators understand that accountability, decisiveness, and command over detail — including the financial details — are crucial to thriving within an organization.

With New Economy CPA’s remote accounting services as part of your EOS model, you have a partner that provides the financial clarity and support needed to not only meet your company’s growth objectives but exceed them.

At New Economy CPA, we believe that Integrators, equipped with accessible, actionable, and accurate financial data and insights, can reach unprecedented levels of success.

Integrators are invited to embrace the robust, strategic partnerships that remote accounting services can offer, bolstering their ability to lead with vision and precision.

https://neweconomycpa.com/wp-content/uploads/2024/10/NewEconomyG1-scaled.jpg13382560Mallory Raberhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngMallory Raber2024-10-22 09:50:552024-10-22 10:46:57How to Thrive as an EOS Integrator: Blending Leadership and Financial Insight

EOS Data can be a tool that unlocks profitability in your business, and aligns your entire team around a shared vision.

Data is the foundation from which all business planning, growth and decision-making is built upon. Without a good foundation, a business will lack accountability, striving for answers in a sea of unknowns.

Check out this recent video from our founder Jeff Allain, and discover how EOS data can transform your business.

In a world where entrepreneurs and business leaders constantly strive for efficiency and growth, EOS data is where continuity is found.

If you’re not familiar with EOS, here is a quick background.

EOS is the Entrepreneurs’ Operating System, designed to provide an encompassing framework to align an entire business. It consists of the following components:

Vision

People

Data

Issues

Process

Traction

Today, we’re focusing on data, because it’s the mechanism used for accountability and making adjustments when something is off track. Without data, there is no way to examine whether the organization is following its vision or goals.

Understanding EOS and Its Importance

EOS is all about moving goals from just an idea into something practical and tangible in the real world.

This pragmatism fosters a culture of accountability and transparency, which is essential for any organization aiming to scale.

The EOS framework encourages businesses to establish a scorecard that tracks key performance indicators (KPIs).

This scorecard serves as a vital tool for measuring progress and identifying areas for improvement.

By having a clear visual representation of their metrics, companies can make informed decisions rather than relying on gut feelings or anecdotal evidence.

The Role of Data in Business Decision-Making

Data is the lifeblood of any successful business. This means access to accurate and timely financial statements, which provide insights into a company’s performance.

These statements should not only reflect past performance but also serve as a predictive tool for future growth. Without this data, entrepreneurs may find themselves making decisions based on incomplete or outdated information, leading to potential pitfalls.

A critical tool to ensure success is cash flow forecasting, particularly the 13-week rolling forecast.

This tool allows businesses to anticipate cash flow needs and make proactive adjustments to their financial strategies.

By forecasting cash flow, companies can avoid unexpected shortfalls and ensure they have the necessary resources to seize growth opportunities.

The integration of these data components into the EOS framework will bring the entrepreneurs’ vision to life.

Implementing the EOS Data

Many companies struggle with the financial side of their operations, often lacking the necessary tools and processes to manage their data effectively. Every business has goals of some kind, even if they’re not explicitly stated.

What’s lacking is a framework for systematically achieving those goals.

In order to do that, the goal must be tied to a number.

Then, you track progress toward that number (in a scorecard) and stay vigilant about tracking progress. If things are off track, you’ll see it, and be able to adjust.

This is the power of data.

You are now able to build a data-driven vision, then work backward from that goal and take consistent action toward your vision.

Your financial models serve as a roadmap, allowing them to set realistic goals and measure progress towards achieving them.

Additionally, having a dedicated implementer who understands the nuances of EOS can significantly enhance a company’s ability to leverage data for strategic decision-making.

The Impact of Data-Driven Decision-Making on Growth

Do you want your business to grow? Do you have a plan for this growth? Unfortunately, growth doesn’t happen by accident. With data-driven decision-making and planning, you can start to take control of your growth.

This proactive approach not only enhances operational efficiency but also fosters a culture of innovation and continuous improvement.

What would that do for your business?

For many, the impact of setting clear goals, then building a data-driven roadmap for achieving them can truly be life-changing.

If you want that roadmap, it starts here. And it starts with data.

EOS provides a structured framework for businesses to align their goals and operations.

Accurate financial data, including scorecards and forecasts, is crucial for informed decision-making.

New Economy CPA specializes in sitting in the Finance Seat to help run the data component of EOS.

The integration of data management can lead to greater control and growth for entrepreneurs.

Let’s Grow Together

The journey to becoming a data-savvy organization may seem daunting, but with the right guidance and tools, entrepreneurs can unlock new levels of success.

That’s what New Economy CPA is here to do – equip entrepreneurs with the tools and guidance they need to walk this journey. We’re walking it ourselves, and are here to help others do the same!

https://neweconomycpa.com/wp-content/uploads/2024/10/New-Economy-2.png6301200Mallory Raberhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngMallory Raber2024-10-10 15:22:052024-10-10 15:22:05Unlock the Secrets of Effective Leadership with EOS Data

It’s always good to approach your business with curiosity.

What’s driving you?

How’s your team doing?

What could be going better?

But sometimes we don’t ask the right questions about our finances, because it can feel a bit intimidating. Who knows what we’ll uncover?

There’s no need to be worried. Knowledge is power, and we’re here to make you more powerful than ever before.

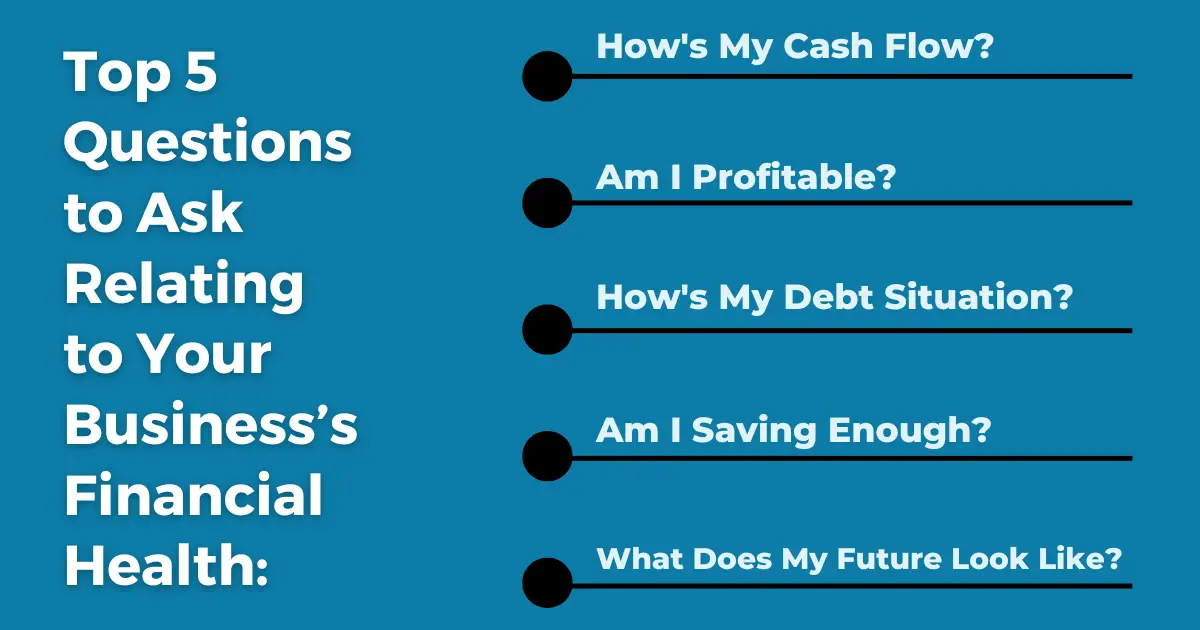

We’ve put together five key questions that will help keep your business on track and grow to new heights.

Leading with Curiosity

There’s a reason the wisdom of Socrates carries on today. He’s famous for asking questions. It’s a method that can help you reach useful insights.

A toga is not required, but certainly, a fun addition if you want to really get into it! 😉

Anyways.

Consider employing the “5 Whys” Method, which is popular among lean startups.

Whenever you think you have an answer to the below questions, try asking “Why?” again and again. You may discover some interesting root causes, causality, and insights.

Always pursue this approach without judgment. Even if it’s tempting to do so, the goal is insights and not blame.

5 Whys Example

The “why” to many of these could have many answers taking you in different directions to explore, but here’s a simple example with one answer and follow-up question for each.

Why aren’t we profitable yet?

Our revenues aren’t exceeding our expenses.

Why aren’t our revenues exceeding our expenses?

Our expenses are reasonable, so it must be that we need to work on our revenue model.

Why isn’t our revenue model working?

We’re not sure, perhaps there’s some more research that needs to be done here. However, it’s based on assumptions from two years ago when we started, and we’ve learned a lot since then which could be updated.

Why haven’t we updated our revenue model?

We get caught up in the hustle and bustle of daily business.

Why are we too caught up in the hustle and bustle of daily business?

We haven’t created a process that includes scheduled time and accountability for strategic thinking and updates.

Okay, here are some good questions to get the curiosity going!

Question 1: How’s My Cash Flow?

Cash flow is the lifeblood that keeps everything running smoothly.

Unlike profit, which is a measure of your earnings over time, cash flow is the actual money flowing in and out of your business right now. If you’re not paying close attention to your cash flow, you could be headed for trouble, even if your business is profitable on paper.

Signs that your cash flow might be struggling include:

Late payments from customers

Overstocked inventory

Unexpected expenses

To keep your cash flow healthy, make sure you’re invoicing promptly, negotiating favorable payment terms with suppliers, and keeping a close eye on your expenses.

Question 2: Am I Profitable? (And If Not, Why?)

This seems like common sense, but it’s key.

While cash flow is essential for short-term survival, profitability is the key to long-term sustainability. It’s the difference between making money and just breaking even.

To figure out if you’re profitable, take a close look at your revenue and your expenses.

Are you pricing your products or services correctly?

Are your costs under control?

Is your sales volume high enough?

Answering these questions and keeping an eye on your budget can help you pinpoint areas where you can improve your profitability.

Question 3: How’s My Debt Situation?

Not all debt is created equal. Some debt, like a loan used to purchase equipment or expand your business, can be a good thing. In fact, we recently wrote an article which will help you get a bank loan for your business.

However, too much debt can weigh your business down with interest payments and limit your cash flow.

If you’re carrying a lot of debt, consider strategies like consolidation or refinancing to reduce your interest rates and monthly payments.

Question 4: Am I Saving Enough?

Even if your business is doing well right now, it’s important to prepare for the unexpected. A rainy day fund can help you weather tough times, like a sudden economic downturn or an unexpected expense.

It can also give you the flexibility to take advantage of new opportunities, like expanding your business or investing in new technology.

Make sure you’re setting aside a portion of your profits each month to build up your savings.

Question 5: What Does My Future Look Like?

Having a clear vision for your business’s future is essential for making smart decisions today. Financial forecasting can help you anticipate potential challenges and opportunities down the road.

By using tools like financial modeling software or seeking the help of a professional advisor, you can develop a roadmap for your business’s financial future.

This can help you make informed decisions about everything from hiring new employees to expanding into new markets.

3 Key Takeaways:

At New Economy, we’re always asking questions and coming up with helpful solutions. We want to help you flourish by taking control of your finances. Here are 3 key takeaways:

Stay Curious: Instead of making assumptions and judgements, keep an open mind and question the world around you.

Keep Asking Why: Go deeper and deeper to see if you can find and solve root causes.

Plan Ahead: Use questions and forecasting to make informed decisions about your business’s future.

Remember, asking the right questions is the first step to taking control of your business’s financial health.

Don’t be afraid to seek help from a financial professional if you need it. By staying informed and proactive, you can set your business up for long-term success.

New Economy Team Members are Experts in Accounting for Entrepreneurs

If you need help asking the right questions, getting your finances organized, and decreasing your taxes, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/07/New-Economy-1.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-07-30 14:45:302024-07-29 14:52:15Top 5 Questions to Ask Relating to Your Business’s Financial Health

Got a vision for business growth that’s bigger than your wallet?

It might be time to make friends with the bank.

Or, at least, become much better acquainted!

Today, we’re breaking down key tips for getting your business funded with a bank loan.

Put on your dress shirt, shine your shoes, and let’s build a funding relationship with your bank.

At New Economy, we’ve helped our clients raise over $75 million in capital.

For many of our clients, raising capital wasn’t about pitching to fancy VCs (venture capitalists).

It was landing a tried-and-true, humble bank loan.

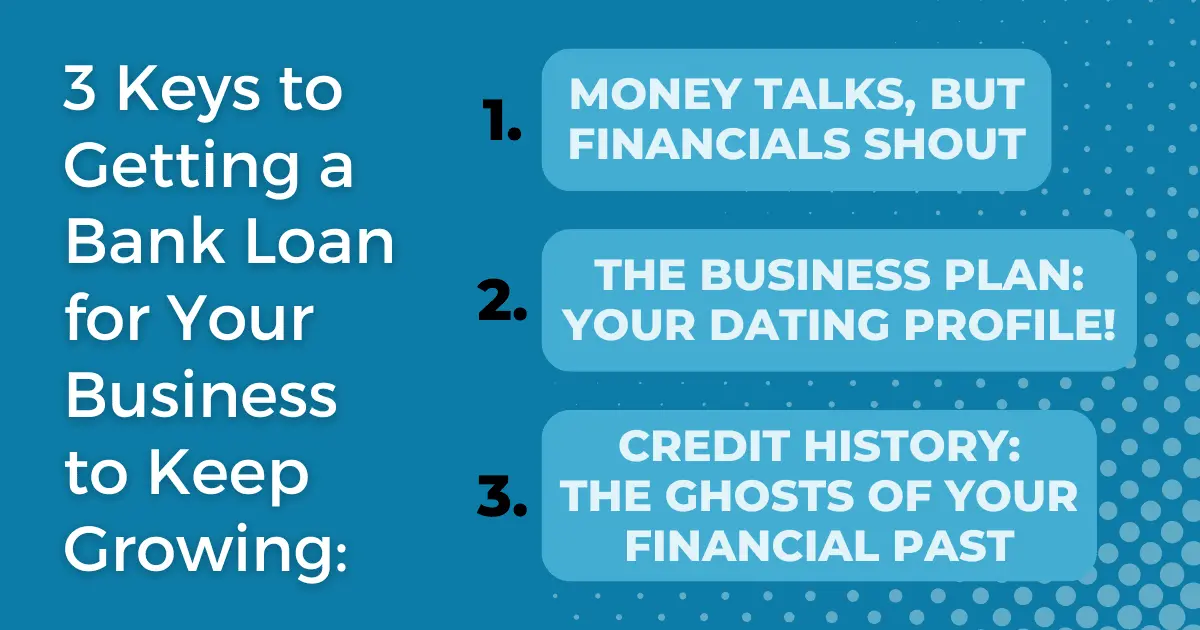

We’ve found these three keys to securing a loan to grow your business:

Organized, Persuasive Financials

A Strategic Business Plan

Knowledge of Your Credit History

Let’s turn those dreams into dollars!

Key 1: Money Talks, But Financials Shout

Don’t let the word “financials” scare you.

It’s your business’s story, but with numbers instead of words.

Here’s what lenders are really looking for:

Healthy Business, Not Lottery Ticket: Show them you’re not a one-hit-wonder, but a sustainable, profitable venture who is prepared for the long haul.

Financials Are Your Resume: Your Profit & Loss statement, Budget, and Balance Sheet are your business’s resume. Make sure they are clean and up-to-date.

Pro Tip: Organize your records like your business depends on it. Because in many cases, it does!

Key 2: The Business Plan: Your Dating Profile!

Think of your business plan as a first date with the bank.

You need to woo them with your vision, strategy, relationship experience, confidence, and potential.

Your Love Letter: Tell them what your business is all about, why you’re so passionate about it, where it’s headed, and why they should invest in your love story.

Show Off Your Smarts: Market analysis, competitor research – prove you’ve done your homework and know your stuff.

Financial Projections: Show them the money – the money you’re going to make them with your brilliant business.

Pro Tip: Be ambitious, but realistic. Lenders love a visionary who’s also got their feet on the ground.

Key 3: Credit History: The Ghosts of Your Financial Past

Your credit history shows highlights (and lowlights) of your past money adventures.

A history of bad credit doesn’t necessarily exclude you from a loan, but you need to demonstrate you’ve since taken responsible action to set things right.

Work towards paying off any debts and building back up your credit score, otherwise, they’ll come back to haunt you.

Some banks will have strict criteria for what they’ll allow historically for someone to be eligible for a loan, but others are flexible, especially if you’re able to win them over with your current financials and business plan.

Remember that both your personal and business credit histories will be considered when applying for most bank loans.

Pro Tip: Check your credit report before you apply for a loan. It’s better to face any financial ghosts now than have them surprise you later.

Reminder: Shopping Around is Okay!

You don’t need to limit yourself to your current bank. It can take a bit more effort to find a new place for a loan, but each has its advantages.

Pros of Getting Loans from Your Current Financial Institution

If you already have a good working relationship, it may be easier for you to manage communication channels, and know what to expect.

Your “home” bank may have discounts for long-standing clients.

It can be a real sanity saver to have all your finances in the same place.

Pros of Shopping Around

You might find some favorable rates and terms for new banks looking to woo you.

Some banks will be more flexible in terms of offering loans if your credit isn’t stellar.

You may find a new bank with incredible customer service, and decide to switch all your banking over at some point (that may be part of their “evil” plan, after all!).

Some online lenders are extremely convenient and price-effective (but do your homework to ensure you’re not being scammed).

3 Key Takeaways

At New Economy, we want to help you flourish by taking control of your finances and getting the financing you need. Here are 3 key takeaways:

Make sure your financials and business plan are organized and showing your growth and potential.

Become familiar with your credit history so you don’t scare your lenders.

Shop around and don’t forget about credit unions! You may find some more favorable rates and terms.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

https://neweconomycpa.com/wp-content/uploads/2024/07/308.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-07-02 11:00:342024-07-02 11:02:493 Keys to Getting a Bank Loan for Your Business to Keep Growing

Are you leaving money on the table by undervaluing your products?

Or are you potentially driving your target customers away with higher prices?

Your financial data can help reveal the sweet spot – the price point that maximizes both sales volume and profit margins.

Negotiate like a pro

Financial data empowers you to become a stronger negotiator with vendors and suppliers.

By understanding your cost structure and past purchase history, you can confidently negotiate better deals, squeezing unnecessary expenses and boosting your bottom line.

Strategy 2: Turn Forecasts Into Cash Flow

Using your financials to create forecasts helps you prepare for stormy seas.

But forecasting is only half the battle. You must then adjust your sails accordingly, or the effort will be wasted.

Here are some examples:

Your forecast predicts a surge in sales during the holiday season.

Instead of investing in a new marketing campaign right now, focus on optimizing your inventory management and staffing levels.

This will ensure you have enough supplies and crew on board to handle the influx of customers and avoid stockouts, which can leave money on the table.

Your forecast predicts a surge in demand for a specific product line.

Reallocate resources from underperforming areas to invest in marketing and production.

This hidden gem may soon become your most profitable product line.

Your forecast predicts an economic downturn in the coming months.

Instead of launching a new product line that requires a significant upfront investment, you can focus on tightening your budget.

Renegotiate contracts with suppliers, or offer discounts to boost sales and maintain cash flow during the rough weather.

At New Economy, we re-forecast our financials weekly! It’s a simple process that takes about 15 minutes, where all department leaders discuss and revise based on any material changes we’ve noticed.

Strategy 3: Reduce Waste and Streamline Operations – Plugging the Leaks in Your Ship

Any captain worth their salt knows even the sturdiest ship can sink from a tiny leak.

Inefficiencies and waste within your business can be pesky leaks, slowly draining your profits.

But fear not, matey!

Financials help you identify and patch those leaks before they become a major catastrophe.

Every penny saved is a penny earned, and financial data empowers you to become a swashbuckling cost-cutter.

By analyzing your financial statements, you can pinpoint areas where expenses can be minimized or eliminated, ensuring your treasure chest remains overflowing.

Chart a course for lean operations: Financial data can reveal areas of unnecessary overhead costs. By analyzing expenses, you can identify potential areas for streamlining operations, such as eliminating redundant subscriptions or renegotiating service contracts.

Mind yer inventory! Inefficient inventory management can lead to overstocking, which ties up your valuable resources. Financials can help optimize your inventory levels, ensuring you have enough supplies on board to meet customer demand without unnecessary stockpiling.

Embrace the power of automation: Financial data can highlight repetitive tasks that are ripe for automation, causing a drain on your team’s time and energy. Freeing up your crew allows them to focus on higher-value activities.

3 Key Takeaways

At New Economy, we help you use financials to make more money and better business decisions.

Here are 3 key takeaways.

Unearth Hidden Profits: Financial data is your treasure map, guiding you towards hidden opportunities within your business. By analyzing key metrics like sales data, cost structures, and customer behavior, you can identify areas for increased profitability.

Chart Course with Forecasts: Financial data empowers you to create forecasts, acting as your compass in uncharted waters. These forecasts help you regularly adjust your sails for stormy seas or fairer weather.

Plug the Leaks: Analyze financial statements to pinpoint areas of inefficiency and waste, like unnecessary overhead costs or bloated inventory levels. Every penny saved is a penny earned!

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/05/298.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-05-28 15:25:272024-05-28 15:26:263 Ways to Use Your Financials to Make More Money

The team thinks you’re just one marketing campaign away from surpassing your goals this year.

But can you do it?

How much can you realistically invest in this campaign without jeopardizing other areas of your business?

At New Economy, we use financial data to make nearly every decision.

It’s guided us to the growth we are seeing today.

So, it’s said with confidence and experience when we say:

Without timely and accurate financial data, you can’t answer your business’s most pressing questions.

Of course, intuition has its place.

But fuel your gut with delicious data to ensure your decisions have a foundation for success.

Timely and accurate financial information is the cornerstone of smart business decisions, big or small.

In this article, we’ll explore the reasons why every business, regardless of size or industry, needs up-to-date and reliable financial data to thrive.

Reason #1: Make informed decisions with confidence.

Reason #2: Navigate challenges and opportunities effectively.

Reason #3: Gain a competitive edge and secure funding.

Before we jump in, ask yourself these reflection questions:

Do you feel confident making strategic decisions based on your current financial information?

Are you prepared to react quickly and effectively if a sudden market shift impacts your business?

Have you ever missed out on a potential business opportunity because you lacked clear financial insights?

If you were to seek funding for your business today, are you confident your financial information accurately reflects its true potential?

Ready?

Reason 1: Make Informed Decisions with Confidence

Do you ever feel like you’re navigating your finances in the dark?

At New Economy, we understand how a lack of direction can keep an entrepreneur up at night.

But think of financial data as a compass – guiding your decisions and keeping you headed toward success.

With timely access to your financial information, you can:

Track progress towards goals by measuring how your current performance compares to your budget and identify areas exceeding or falling short of expectations.

Identify areas for improvement by analyzing trends in sales, expenses, and profitability.

Make data-driven decisions instead of relying on guesswork.

Let’s revisit the marketing campaign from the beginning of this article.

By analyzing past marketing data, you can see which strategies brought the best return on investment (ROI).

This allows you to allocate your budget more effectively for the upcoming campaign, maximizing your chances of success

Reason 2: Navigate Challenges and Opportunities Proactively

We all know to expect the unexpected as entrepreneurs!

Whether it’s a global pandemic, supply chain disruptions, or a strangely eventful pop culture event…

there’s no crystal ball to prepare us for the future.

But, smart businesses can still be reasonably prepared for the future with timely and accurate financial data.

It lets you pivot at a moment’s notice.

You can mitigate potential damage or explore a new opportunity with the click of a button if you’ve got the right data on your dashboard.

Here’s how:

By analyzing trends and historical data, you can identify potential financial risks and develop contingency plans to mitigate their impact.

Having a clear picture of your current financial situation allows you to react quickly to unexpected events and adapt your strategies accordingly.

Timely financial data can reveal new market trends or opportunities you might otherwise miss. This allows you to capitalize on these opportunities and stay ahead of the competition.

Now, back to the marketing campaign.

Your sales data starts showing a decline in a specific product category just before launch.

You realize it’s showing a shift in a market trend.

Thanks to the early warning, you can do some research to identify the causes.

Then you can adjust your campaign messaging or even pivot your marketing strategy to target a different product line that’s experiencing higher demand.

Reason 3: Gain a Competitive Edge and Secure Funding

Financial health is a top priority for investors and creditors.

Regardless of the type of funding you seek, your financial health will be reviewed thoroughly before getting anywhere near the purse strings.

Timely and accurate financial data can be a key indicator of your business’s growth potential and ability to repay loans.

Here’s why:

Up-to-date financial statements give a clear picture of your company’s financial performance, profitability, and debt levels. This builds trust with investors.

Financial data can be used to create forecasts and projections for future growth. This allows you to showcase your company’s potential to generate strong returns for investors.

Your funders love when you can answer questions with accurate financial data that was generated recently, instead of bumbling about how they’ll need to wait a few weeks for you to get the data to answer their questions.

A solid understanding of your financial position empowers you to negotiate more favorable terms with lenders and suppliers.

Beyond attracting funding, reliable financial data also helps you stay competitive:

Set competitive prices while maintaining healthy profit margins by analyzing your cost structure and customer behavior.

Gain a clear financial picture to make informed decisions about resource allocation, investments, business expansion, and more.

Let’s come back to our marketing campaign.

You’ve crunched the numbers and decided you just can’t risk dipping into your business savings to launch a massive marketing campaign.

The team decides taking out a short-term, low-interest loan could maximize your outcomes and minimize your risk.

By demonstrating your financial stability and growth potential with accurate data, you’re in a much stronger position to secure funding for the campaign.

When you share how you made your decision to pivot the focus of your marketing campaign based on the most recent data, your funder feels more confident you’re making decisions based on real-world data.

3 Key Takeaways

At New Economy, we want to help you gain control of your finances to make smart decisions.

Part of that is understanding your finances and how to drive business performance.

Here are 3 key takeaways.

Make informed decisions with confidence. Timely and accurate data means you have a more complete picture of your business.

Be prepared for challenges and opportunities. Being able to see your financial records quickly means you can change direction when the time is right.

Secure funding and gain a competitive edge. Showcase your company’s financial position with ease, preparing you for investment, loans, and the ability to gain a competitive advantage.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If collecting timely and accurate data is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/05/287.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-05-15 11:43:152024-05-15 11:45:533 Reasons Every Business Needs Timely and Accurate Financial Data

At New Economy, we hit our measurables of revenue of $614K, gross profit of 50%, and net profit of 12%.

Also, we hit 80% of our rocks. These are the top priorities for us in the quarter.

What did you learn?

At New Economy, we learned a lot.

We learned that we need to keep making financial investments in our team members through training and growth opportunities.

We also learned we need to increase our financial investments in marketing to help let entrepreneurs know we are here to help them gain control of their finances to make smart decisions.

But what do we do with these learnings from a financial perspective?

At New Economy, we believe you can use this information to forecast for the next quarter.

For a bit of background on creating a budget, check out our blog posting Here.

Your financial budget is set for the and will not change.

However, your financial forecast can change based on what you have learned.

In this article, you will learn about:

The difference between a financial budget and a financial forecast

When and why to update your financial forecast

Top 3 Takeaways

Let’s dive in.

The Difference Between a Financial Budget and a Financial Forecast

Most Companies, including New Economy, perform their financial budgeting towards the end of the year.

Being a December year-end, we typically begin the process in November and wrap up in the first week of January.

The financial budget is the goalpost – think football and field goalposts. You are aiming to kick the ball through the goalposts to score. Or from a financial point of view, achieve the budget which keeps you on the path to achieving your overall goals.

You are estimating things like the investments you need to make into the business that will get allocated to hiring, marketing, and operating expenses.

Further, you are determining your revenue goals and the direct costs to support that revenue.

It is your best guess.

You are painting the financial road map month to month to help you achieve your annual financial goals.

It’s important to note that your budget should not change.

You don’t want to move the goalposts.

We call that cheating 🙂

However, there is another very helpful tool.

It is your financial forecast.

Your financial forecast is identical to your budget. It is set up the same way, looks the same and even works the same.

The biggest difference is you can change your financial forecast.

In fact, at New Economy, we are constantly changing our forecast.

But we are also continuously lining up the financial forecast against the financial budget.

The idea is the financial forecast is updated for what is happening in the business, and in our experience that is lots of change.

At the end of the day, we hold ourselves accountable to the financial budget that was set and use the financial forecast as the real-time road map to get to the intended destination.

It’s kind of like the direction app, Waze.

You enter your destination and ways will give you the directions to get to your destination. This is like your financial budget.

However, then an accident happens.

Waze then recalibrates and provides an alternate route. There are changes but it will still get you to the original destination. This is like your financial projection.

So, we suggest you make sure you have a financial budget.

Then modify that budget by bringing it alive based on changes or real-time information and call that your financial forecast.

In the next section, we will talk about when and why to update your financial forecast.

When and Why to Update Your Financial Forecast

When to change your forecast

By now you should know the difference between a financial budget and a forecast.

The next question is when do we update the financial forecast?

There is a wide range of answers to this question depending on:

The business

The visibility required

The investment of time that’s willing to be made

We have some customers that re-forecast weekly.

They have built a weekly process around this and have determined that weekly forecasting gives them real-time insights that they need to manage the business.

We have some customers that re-forecast monthly or even quarterly.

They will access real-time changes but more so look at monthly budget versus actual information. When items are on and off track, they will trigger changes to the model.

At New Economy, we re-forecast weekly.

We have created a simple process where all the department leaders provide any material changes. It takes us about 15 minutes per week to do this and we will discuss why we do it this way in a bit.

In any case, updating on a weekly, monthly, or quarterly basis you are on the right track.

You need to turn your budget into a forecast applying what you have learned.

Why change your forecast

One of our taglines is we help entrepreneurs gain control of their finances to make smart decisions to build and grow their businesses.

To make smart decisions you need timely and accurate financial information like a financial forecast.

The forecast gives you the most accurate picture of how your business is performing from a financial perspective at any point in time.

Having that timely and accurate financial information allows you to do the following:

Determine if you are on or off track to your budget

Identify areas of opportunity or improvement

Run decision-making scenarios that show the financial impact

The reason New Economy updates the forecast weekly is to have good data for our weekly Leadership Team meeting called our Level 10 meeting.

As part of that weekly Level 10 Meeting, we review a weekly, monthly, and quarterly scorecard which has the financial data we’re measuring.

And you guessed it, one of the sources of that data is our financial forecast.

One last thing to note on the financial forecast.

Once a month has closed, we drop the actuals into the forecast. Refer to more information on the financial close here.

For example, if we are through Q-1, the months of January, February, and March would have actual results in the financial forecast. The remaining nine months would be the projected results.

And we continuously analyze the financial forecast against the original budget.

A financial budget and financial forecast are very powerful business tools. So don’t sleep on the importance of implementing them into your business.

3 Key Takeaways

At New Economy, we want to help you gain control of your finances to make smart decisions. Part of that is understanding your finances and how to drive business performance.

Here are 3 key takeaways.

Make sure you have a budget in place. Don’t change the budget once you set it. And build the budget showing details such as monthly and by-line items.

Make sure you transition your budget into a forecast. Your forecast can be updated weekly, monthly, or quarterly. It can be changed and should be compared back to the budget.

Leverage these tools in your business. They are powerful tools to help you achieve your business goals.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/03/258.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-03-27 15:44:482024-03-27 15:47:253 Keys to Turn Your Financial Budget into a Financial Forecast

Full disclosure, we just set up a ChatGPT account.

We are excited 🙂

Here is how ChatGPT defines the month-end close process.

The financial close process, often referred to simply as “the close,” is a series of steps undertaken by organizations at the end of an accounting period to ensure that all financial transactions for that period are accurately recorded and reported. This process typically occurs monthly, quarterly, or annually, depending on the reporting requirements of the organization.

The financial close process involves several key activities, including:

Reviewing Transactions: Accountants review all financial transactions recorded during the period to ensure accuracy and completeness. This includes verifying that transactions are properly classified and documented.

Adjusting Entries: Any necessary adjustments are made to account for items such as accruals, prepayments, depreciation, and other timing differences. These adjustments ensure that the financial statements reflect the true financial position of the organization.

Reconciliation: Various accounts, such as bank accounts, accounts receivable, and accounts payable, are reconciled to ensure that the balances reported in the financial statements match the supporting documentation.

Closing Entries: Temporary accounts, such as revenue, expenses, and dividends, are closed to the appropriate permanent accounts, such as retained earnings. This process resets the temporary accounts to zero in preparation for the next accounting period.

Financial Reporting: Once all adjustments and closing entries have been made, financial statements are prepared, including the income statement, balance sheet, and statement of cash flows. These statements provide an overview of the organization’s financial performance and position during the period.

Review and Approval: The finalized financial statements are typically reviewed by management and may require approval from stakeholders such as the board of directors or external auditors.

Archiving Documents: All supporting documentation related to the financial close process, including journal entries, reconciliations, and reports, are archived for future reference and audit purposes.

The financial close process is crucial for ensuring the accuracy and integrity of an organization’s financial reporting. It allows stakeholders to make informed decisions based on reliable financial information and helps maintain compliance with regulatory requirements. Additionally, a well-executed close process can identify potential errors or discrepancies early, allowing for timely corrective action.

Darn, that was pretty good. Thanks Chat GPT!

Our simple and high-level definition is:

The Financial Close process is a series of steps to help ensure that each month the financial statements are delivered in a timely and accurate manner.

Entrepreneurs and business owners need the financial statements for the following reasons:

Access if the business is on track with its financial goals

Determine the financial health of the business

Have data to make smart decisions

Now we have an understanding of this process and why it’s important.

Let’s jump right into 5 Keys to make it awesome.

5 Keys to an Awesome Financial Close Process

Here are 5 important considerations to create an awesome close process.

Key #1 – Make sure there is a month-end close checklist.

We love checklists. They provide clarity around the steps that need to be performed to get the desired outcome.

For the desired outcome to be accurate financial statements then some steps need to be performed to accomplish that desired outcome.

Let’s look at Chick-fil-A as an example, since we love their chicken sandwiches.

Whether you go to a Chick-fil-A in Rhode Island or California your spicy deluxe chicken sandwich will taste the same, take the same amount of preparation time, and be delivered with a smile.

Why?

They have checklists covering the various components of preparation and service. And they do this at scale.

So relating to the month-end close here are a few examples of items that should be on that checklist.

Bank Accounts

Ensure all transactions are properly flowing into QBO

Ensure all transactions are properly coded to the proper GL account

Ensure that the bank reconciliation is prepared

Ensure that the reconciling items are identified around outstanding checks

Ensure that the reconciling times are identified around deposits in transit

Fixed Assets

Ensure that assets purchased over $1,000 are capitalized

Ensure depreciation is booked on all assets each month

Ensure that assets no longer being used are removed

Ensure that your depreciation schedule agrees with your balance sheet

Ensure that your depreciation expense agrees with your profit and loss statement

Ensure that repairs and maintenance are properly expensed in your profit and loss

An accountant at the staff level should be able to perform the above procedures to ensure that the accounts are properly stated on any balance sheet.

This can be replicated each month and over many types of accounts.

You get the point, the checklist allows for scalability just like the chicken sandwich in different states at different store locations. Yummy.

Key #2 – Make sure you create accountability and set due dates.

This one is very important.

It is simple yet at the same time complicated.

Take the above example and apply it to bank accounts.

We can simply create accountability by assigning those steps to Tom with a due date by the end of the second week.

That’s pretty clear and straightforward. The complexity comes into play when Tom gets sick or information is not ready.

The key here is to manage well, be flexible, communicate new due dates, and hold the line on accountability.

Here are some of the challenges we see that are easily avoidable:

No one is a named owner of the task

There are multiple owners of the task, thus no owner

There is no set due date

If expectations change, there is no new due date set

There is no conversation around accountability for missed deadlines

Keep in mind how important this is.

The reason for our month-end close process is to deliver timely and accurate financial information and if Tom is not timely, our goal will be missed.

The answer here is to lead, manage, and hold Tom accountable.

Key #3 – Establish a quality control review of the financials.

Ok, so the checklist is complete and Tom has met all his deadlines.

Now we are onto the quality control process.

Remember, Tom is a staff accountant. His work needs to be reviewed and checked by Jerry the Quality Control team member.

Since we are using financial statements to make smart decisions, we want to make sure the financials are reviewed by an experienced team member.

This goes back to steps #1 and #2.

A checklist should be prepared for the quality control reviewer to perform.

Further, Jerry should have deadlines as well and should be held accountable so that we can meet the desired outcome.

It could create some real pain around cash flow if an entrepreneur makes bad decisions due to relying on bad financial statements.

A quality control review is a good investment in making good decisions.

Key #4 – Establish a month-end close meeting where the financials are reviewed.

This is one of our favorite meetings at New Economy.

Here we get to focus on our core value of delivering awesome service.

We schedule 30-minute monthly zooms to provide our entrepreneurs with financial results from the month and LOTS of knowledge that we derive from the financial statements is spoon-fed to our customers.

Here are some examples of what we discussed during the close meeting:

Budget versus actual results by line item with a narrative

Cash burn for the month

Reporting on KPIs with the narrative

Focus on spend management

Connect actual results to financial goals

It’s pretty fun to tease this information out of the financial statements.

We are providing visibility and information on changes needed in the next month, based on the learnings.

Key #5 – Apply what you are learning during the financial review.

Don’t get me wrong.

There is a lot of work in steps #1-#4.

But the real magic happens here.

After that month ends, the big question is “What did we learn?”.

Maybe we learned in our budget versus actual analysis that we are overspending on software costs. This is causing us to be off track from our goals.

Our advice is to dig in.

Is this overspending going to keep happening? Do we have to shut it down? Was it a one-time thing and it will fall back in line next month with some underspending?

I think you get the point.

There is a lot of learning in the financial statements that have action items that can improve the financial performance of the business.

This is gold for any entrepreneur.

And you don’t need a full-time accountant to pull this off.

At New Economy, we want to help you gain control of your finances to make smart decisions. Part of that is understanding your finances and how to drive business performance.

Here are 3 key takeaways.

Make sure you have a monthly close checklist. It should be written and updated quarterly. This will help you get to the desired outcome. Further, if you and your accountant should part ways you have a road map for performing the month-end close specific to your business.

Make sure you are clear with deadlines and hold your team accountable. This is key to getting timely financial results. And you are also striving for accuracy so setting up a monthly quality control review is important.

Once you get your financial statements, use them. Learn how to read them. Learn what they are telling you about your business. And then go take that learning to improve the financial condition of your business.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

Having the right accounting and finance team is important.

Really important.

Why?

Contrary to popular belief, your accounting team is not just overhead.

You need timely and accurate financial information to make smart decisions to build and grow your business.

At New Economy, we think about the right seats needed to support the accounting department for any business. Then we think about getting the right people in those seats.

Most small businesses need some form of an Accountant, Controller, or CFO.

It really depends on the type of business, the stage the business is in, and the growth plans the business has for the future.

And each of these seats has a different skill set and value they bring. It goes from tactical to strategic in nature.

But what are the signs that your accounting team is not working?

In this article, you will learn about:

The top reasons your accounting set up is no longer working

5 ways to tell it’s time to change accountants

Top 3 Takeaways

Let’s dive in.

The Top Reasons Your Accounting is No Longer Working

There are several reasons why this can be the case but here are a few.

Reason #1 – Sorry, You really don’t have an accountant.

Very early on in the life of your business, you might have had Tony’s aunt doing the accounting.

There is nothing wrong with Tony’s aunt. However, she is self-taught and doesn’t fully understand what she is doing. Sure, she can pay bills and is wicked cheap, but she’s just a family friend, not an accountant.

This is common and ok, but this will hold you back if you don’t make a move.

Reason #2 – The business outgrew your current accountant.

You have a vision of where you want to be. You are chasing down that vision and raising capital, hiring people, building processes, and executing your plan.

Your business is growing and evolving, and when that happens things can get complicated in the various departments, such as your accounting department.

But your current accountant is stuck in the old way of doing things. They don’t have a grown mindset and they are not open to technology and new ways of doing things.

This results in delays and inefficiencies because the business is growing but your accountant is not growing with it.

This too will hold you back.

Perhaps you have a good tactical person but need to layer on a more experienced person who focuses on strategy from an internal perspective.

Reason #3 – Your accountant is overhead and is doing too many administrative tasks.

Many internally placed accountants get very comfortable and are overpaid.

Yup, I said it.

They have a high-level technical skill set and are compensated for it.

But they are given tasks that don’t relate to this skill set. They start doing administrative work, they get pulled into a bit of human resources or even managing technology.

They get pulled in too many directions, are overpaid, and are no longer adding value.

They become overhead as opposed to an investment that is helping you get closer to achieving your goals.

Reason #4 – You don’t need a full-time accountant.

Once you really dive into point #3, you may realize that you don’t need a full-time accountant.

How can this be?

You have them focus on the functions that require their specialized skill set. Nothing more, nothing less.

Also, as part of not needing a full-time accountant, you can save money. You are not covering insurance, benefits, training, or even internal time to manage this person. We believe the cost of a part-time remote accountant can be a big savings with a better return on your investment.

Financial statements – Within 20 days of month end

Budget vs Actual reporting – Within 20 days of month end

Forecasting – Updates within 20 days of month end

Having timely information is important. You want to make real-time decisions based on data that is current.

Reason #2 – You are not getting accurate financial information.

If you are not getting accurate financial information a red flag should go up. The information is the same as that listed above.

But how do you know it’s accurate considering you’re not an accountant and an entrepreneur?

Here are some thoughts:

Use your gut, it got you this far

Share the information with a peer group and compare information

Ask a trusted advisor or mentor with a financial background to have a look

Timely and accurate information are the keys to making smart business decisions.

Reason #3 – You keep getting surprised and are not learning from the past.

No one likes surprises.

So if you’re looking at your budget versus actual reporting and are surprised when something is off track, a red flag should go up.

Or if you get to year-end and your monthly financials that have been reported on change, a red flag should go up.

Or if you are caught off guard by an unexpected tax bill, a red flag should go up.

Things change fast in business, but learning and applying is key.

Remember the old saying “Fool me once shame on you but fool me twice shame on me”?

Reason #4 – You can’t see into the financial future.

Your historical statements are very important.

As we stated, they need to be accurate and delivered on time.

But we also need windows out into the future from a financial perspective. So if you can’t see out into the future whether it be 13 weeks of cash flow into the future or 24 months of your profit and loss out into the future, a red flag should go up.

Reason #5 – You are frustrated and feel pain and confusion on the financial side of your business.

We have said it before, trust your gut. You have great intuition.

So if even hearing the word financials causes you to feel pain or frustration, a red flag should go up.

Or if your accountant is confused and can’t seem to give you straight answers, a red flag should go up.

So there you have it; 5 examples that can give you an indication it’s time to think about changing your accounting team.

3 Key Takeaways

At New Economy, we want to help you gain control of your finances to make smart decisions. Part of that is understanding your finances and how to drive business performance.

Here are 3 key takeaways.

Make sure you have the right people in the right seats on your accounting team. Early on Tony’s aunt might have been a great fit. But since you have raised some capital, have 10+ employees, and are on your way to profitability it’s time to increase the firepower of your accounting team.

Make sure you are not flying blind. You should have timely, accurate historical financial statements and visibility into the future financial condition of the business based on your forward-looking projections.

Trust your gut and invest in your accounting and financial team. They are an investment that should help you to get closer to your goals by providing you with invaluable insight to make great business decisions.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/02/243.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-02-16 10:45:442024-02-16 10:46:585 Ways to Know You Need a New Accountant

Think about the dashboard in your car. You have many gauges and lights that tell you different things going on in your car.

For instance, you have a gas light. If the gas light is on, it’s a warning that you need to fill up your gas tank. If you avoid this you may get stuck and you may not make it to your intended destination.

Or you have an oil light. If this is on and you don’t put oil in your engine, your engine could potentially seize you and you will have a major problem.

This is all good information to have. This information allows you to make good decisions for your vehicle, your primary need for transportation which is very important.

Financial statements are much like the gauges on the dashboard of your vehicle.

They give you information about the financial condition of your business.

We run into many entrepreneurs who don’t know how to use this important information, and that’s ok, they are entrepreneurs and should be casting vision and building stuff.

However, they should still have a high level of knowledge on how to use financial information to help them get closer to their goals.

In this article, you will learn about:

The three standard financial statements

5 ways to understand your financial statements

Top 3 Takeaways

Let’s dive in.

The three standard financial statements

Pop quiz.

Do you know the three standard financial statements that you should be using to assess the financial condition of your business?

If not, we got you.

They are:

The Balance Sheet

The Profit and Loss Statement

The Statement of Cash Flows

Balance Sheet

Your balance sheet is a statement that will help you to understand the financial condition of the Company.

We all want to know how our business is doing, don’t we?

It shows all of your assets, liabilities, and equity in the business.

Your assets are things like cash, accounts receivable, and fixed assets. They are used to help your business produce future value.

Your liabilities are amounts you owe to third parties in the form of accounts payable. Liabilities can be good if used properly. They allow you to “borrow” as you typically have 30 days to pay the third party.

Long-term bank debt is another form of liability. This can be used for timing issues like making purchases up front that will produce value down the road and allow us to repay the debt.

Lastly, your equity is all of the capital contributed to the business as well as profits and losses accumulated.

Profit and Loss Statement

Your profit and loss statement will help you understand if the core product or service you are delivering is producing a profit.

It is divided into a few sections as follows.

First, you have your revenue and cogs. Your revenue is straightforward and represents your earnings for doing what you do. Your cogs, or cost of goods sold, is variable with your revenue. Meaning if your revenue goes up, it’s likely the costs to produce the revenue go up. The key here is the gross profit.

Next, you move into operating expenses. These are typically fixed expenses and things like rent, marketing, software, and salary expenses.

So if you take your revenue less your cogs less your operating expenses you will get to your profit number.

Cash Flow Statement

Ok, so your cash is driven by profitability. If your Company is producing a profit on its Profit and Loss Statement you are generating cash flow.

The cash flow statement shows all the sources and uses of cash.

As for sources, we simply mean where your cash is coming from. As for uses, we simply mean where your cash is going.

This is a great statement to help you get a handle on how much cash you burned through in a particular month and where it went.

General thoughts on financial statements

Ok, here are some general thoughts on financial statements in bullet form.

These should be produced timely. Typically within 30 days of the end of the month.

These need to be accurate. You need good financial statements to make good decisions.

To get to accuracy you need the right person producing them. Make sure the team member has the right level of experience.

If you are doing $1M or more in revenue, you should consider accrual accounting. It paints a more realistic picture of profitability.

Reflect on these and seek to understand what they are telling you about the business.

In the next session, we will get into ways to understand the financial statements. It requires a pause at month end to really deep dive into them to pull out the “golden nuggets”.

We did write a detailed post on these financial statements here if you want to dive deeper.

5 Ways to Understand Your Financial Statements

We are pretty sure there are more than 5 ways to understand your financial statements.

However, we will cover 5 which should help you better understand how your business is performing.

Let’s take each financial statement one at a time and try to glean some wisdom out of them.

Balance Sheet

The balance sheet of your business will help you to understand the following:

The degree of working capital in the business. Working capital is the business’s ability to meet short-term obligations with current assets. It is an indicator of the business’s ability to collect on receivables, manage inventory well, and leverage accounts payable terms.

For example, Amazon has $100 in current assets and $50 in current liabilities. The working capital for Amazon is $50 ($100-$50).

On the other hand, Facebook has $75 in current assets and $70 in current liabilities. The working capital for Facebook is $5 ($75-$70).

Amazon wins. The higher the working capital, the healthier the business as there is more of a cushion to meet the current needs of the business.

The receivable turnover of the business will help you understand how quickly you are converting accounts receivable to cash. Cash is king, so the faster the better.

For example, Amazon has $500 in net sales and $100 in average receivables. The receivable turnover for Amazon is 5 ($500/$100).

On the other hand, Facebook has $500 in net sales and $50 in average receivables. The receivable turnover for Facebook is 10 ($500/$50).

Facebook wins. The higher the ratio, the healthier the business as cash is coming into the business quicker and the Company is managing collections better.

Profit and Loss

The profit and loss statement of your business will help you to understand the following:

The Gross profit % of the business will help you understand how much profit you earned on the sale of your products or services.

For example, Amazon has $500 in net sales and $100 in Cogs. The gross profit for Amazon is 80%($500-$100=$400 then $400/$500=80%).

On the other hand, Facebook has $500 in net sales and $50 Cogs. The gross profit for Facebook is 90% ($500-$50=$450 then $450/$500=90%).

Facebook wins again. The higher the percentage, the more money is earned on the product sales. It states that for every $1 of revenue that Facebook earns, they get to keep $.90 for profit.

The Net profit % of the business will help you understand how much profit you earned on everything. This includes your fixed expenses.

For example, Amazon has $500 in net sales,$100 in Cogs, and $20 in Op X. The net profit for Amazon is 76%($500-$100-$20=$380 then $380/$500=76%).

On the other hand, Facebook has $500 in net sales, $50 Cogs, and $5 in Op X. The net profit for Facebook is 89% ($500-$50-5=$445 then $445/$500=89%).

Facebook wins again. The higher the percentage, the more money is earned overall in the business. It states that for every $1 of revenue that Facebook earns, they get to keep $.89 for profit.

Cash Flow Statement

The Cash burn rate of the business will help you understand the rate at which your business spends money and the number of months of cash you have available.

For example, Amazon has $100 in cash and spends $50 per month. The burn of 50 per month results in 2 months of runway. ($100/50).

On the other hand, Facebook has $200 in cash and spends $30 per month. The burn of 30 per month results in 6 months of runway. ($200/30).

Facebook wins again. The more months of cash flow the more the business can be supported longer.

Summary of understanding your financial statements

Based on utilizing the financial statements, we were able to understand things like liquidity, profitability, and even cash reserves.

These metrics, driven by the financial statements, help us to better understand how the business is performing.

The beauty of using the financials and these metrics is you can track and compare against yourself to see your improvement. You can even compare yourself against your competitors, industry averages, or your future goals.

No matter what, your financial statements are a great source of helping you understand the financial condition of your business.

And the better the financial condition, the higher the probability of your being able to have the resources to meet your goals and vision.

3 Key Takeaways

At New Economy, we want to help you gain control of your finances to make smart decisions. Part of that is understanding your finances and how to drive business performance.

Here are 3 key takeaways.

Make sure you are getting accurate financial statements within a 30-day period after the month’s end. If you are not sure if your financial statements are accurate, reach out and we can provide you with some feedback.

Take the time to reflect on your financial statements. Determine what they are telling you about the financial condition of your business. Continue to monitor your progress against the historical financial statements and benchmark against competitors.

Do the work. Meaning, if your financial condition is not good or has deteriorated, determine what is driving that and fix it. Go into the business and spend the time getting to the root cause of the issue. The financial statements are just the indicator of something either being on or off track.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/02/241.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-02-06 10:12:262024-02-06 10:15:235 Ways to Understand Your Financial Statements and Get Closer to Your Goals

How Leveraging Financial Data and Your Accounting Team Can Help.

As a growth-stage entrepreneur, you’re constantly dealing with emotional highs and lows based on the various circumstances thrown your way that are not in your control.

We feel your pain.

And we have learned that this can impact the confidence you have in your small business. But what really is confidence?

Here are a few definitions.

It is the feeling or belief that one can rely on someone or something.

Or defined another way, a feeling of self-assurance arising from one’s appreciation of one’s own abilities or qualities.

Or the state of feeling certain about the truth of something.

Which begs the question: Do you have confidence in your small business? And can you increase that confidence in your small business using financial data and leveraging your accounting team?

At New Economy, we believe so.

Why, you ask?

It aligns with our efforts of helping you gain control of your finances to make smart decisions to build and grow your company.

In this article, you will learn:

What types of issues might be eroding your confidence in your small business

What you can do to overcome these issues

Three key takeaways related to improving the confidence in your small business using data

Let’s dive in.

What Issues May be Eroding Your Confidence in Your Small Business?

There are a few important things to discuss here.

First off, there is no silver bullet and the game of business covers a lot of ground. Therefore, we will focus on issues on the financial side of your business, which is the space that we play in. But this approach can be applied to any department such as marketing or even operations.

So what could deteriorate your confidence in your small business as it relates to the financial side of your business?

Maybe it’s people, maybe it’s process, maybe it’s technology, or maybe it’s a combination of all three.

Let’s Talk People

Start with the Right Seats