Got a vision for business growth that’s bigger than your wallet?

It might be time to make friends with the bank.

Or, at least, become much better acquainted!

Today, we’re breaking down key tips for getting your business funded with a bank loan.

Put on your dress shirt, shine your shoes, and let’s build a funding relationship with your bank.

At New Economy, we’ve helped our clients raise over $75 million in capital.

For many of our clients, raising capital wasn’t about pitching to fancy VCs (venture capitalists).

It was landing a tried-and-true, humble bank loan.

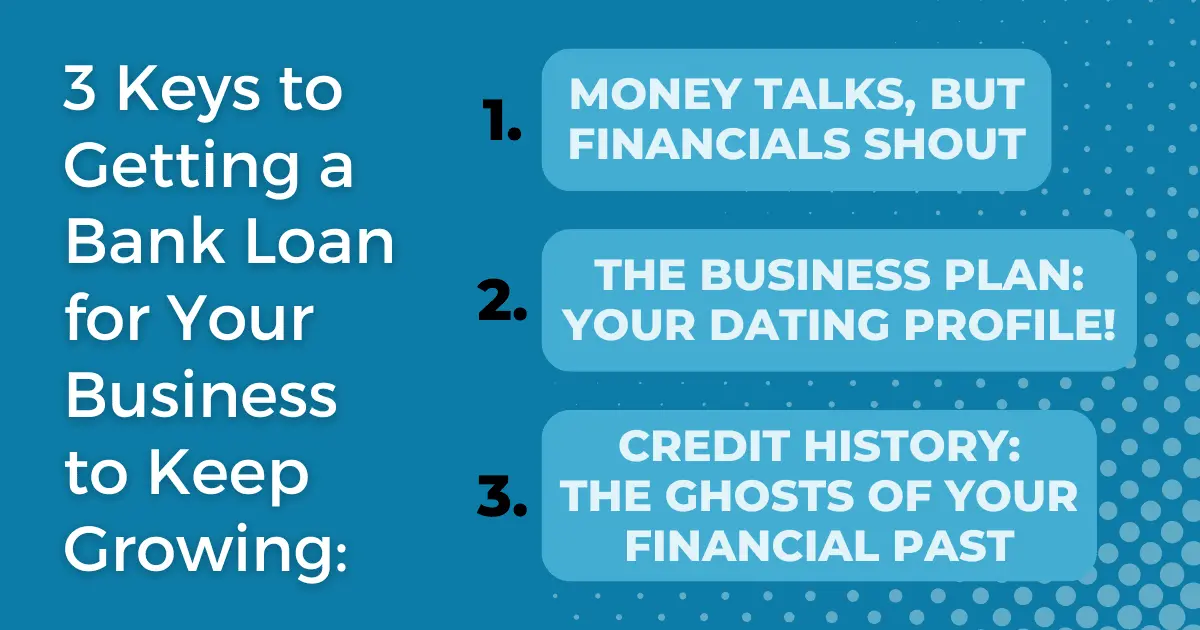

We’ve found these three keys to securing a loan to grow your business:

Organized, Persuasive Financials

A Strategic Business Plan

Knowledge of Your Credit History

Let’s turn those dreams into dollars!

Key 1: Money Talks, But Financials Shout

Don’t let the word “financials” scare you.

It’s your business’s story, but with numbers instead of words.

Here’s what lenders are really looking for:

Healthy Business, Not Lottery Ticket: Show them you’re not a one-hit-wonder, but a sustainable, profitable venture who is prepared for the long haul.

Financials Are Your Resume: Your Profit & Loss statement, Budget, and Balance Sheet are your business’s resume. Make sure they are clean and up-to-date.

Pro Tip: Organize your records like your business depends on it. Because in many cases, it does!

Key 2: The Business Plan: Your Dating Profile!

Think of your business plan as a first date with the bank.

You need to woo them with your vision, strategy, relationship experience, confidence, and potential.

Your Love Letter: Tell them what your business is all about, why you’re so passionate about it, where it’s headed, and why they should invest in your love story.

Show Off Your Smarts: Market analysis, competitor research – prove you’ve done your homework and know your stuff.

Financial Projections: Show them the money – the money you’re going to make them with your brilliant business.

Pro Tip: Be ambitious, but realistic. Lenders love a visionary who’s also got their feet on the ground.

Key 3: Credit History: The Ghosts of Your Financial Past

Your credit history shows highlights (and lowlights) of your past money adventures.

A history of bad credit doesn’t necessarily exclude you from a loan, but you need to demonstrate you’ve since taken responsible action to set things right.

Work towards paying off any debts and building back up your credit score, otherwise, they’ll come back to haunt you.

Some banks will have strict criteria for what they’ll allow historically for someone to be eligible for a loan, but others are flexible, especially if you’re able to win them over with your current financials and business plan.

Remember that both your personal and business credit histories will be considered when applying for most bank loans.

Pro Tip: Check your credit report before you apply for a loan. It’s better to face any financial ghosts now than have them surprise you later.

Reminder: Shopping Around is Okay!

You don’t need to limit yourself to your current bank. It can take a bit more effort to find a new place for a loan, but each has its advantages.

Pros of Getting Loans from Your Current Financial Institution

If you already have a good working relationship, it may be easier for you to manage communication channels, and know what to expect.

Your “home” bank may have discounts for long-standing clients.

It can be a real sanity saver to have all your finances in the same place.

Pros of Shopping Around

You might find some favorable rates and terms for new banks looking to woo you.

Some banks will be more flexible in terms of offering loans if your credit isn’t stellar.

You may find a new bank with incredible customer service, and decide to switch all your banking over at some point (that may be part of their “evil” plan, after all!).

Some online lenders are extremely convenient and price-effective (but do your homework to ensure you’re not being scammed).

3 Key Takeaways

At New Economy, we want to help you flourish by taking control of your finances and getting the financing you need. Here are 3 key takeaways:

Make sure your financials and business plan are organized and showing your growth and potential.

Become familiar with your credit history so you don’t scare your lenders.

Shop around and don’t forget about credit unions! You may find some more favorable rates and terms.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

https://neweconomycpa.com/wp-content/uploads/2024/07/308.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-07-02 11:00:342024-07-02 11:02:493 Keys to Getting a Bank Loan for Your Business to Keep Growing

One of the interesting things is that these statistics remained fairly consistent for the past few decades. That means there’s a lot we can learn from the past years.

Here are the top reasons why businesses fail:

Finances – Especially Cash Flow

Financing Challenges

Minimal Operational Efficiency

Not Focusing on The Customer and Evolving Marketing Trends

Lack of Effective Business Vision, Strategy and Execution

Finances – Especially Cash Flow

According to SCORE, a whopping 82% of small business failures can be traced back to cash flow issues.

That doesn’t mean the business isn’t profitable. But without the cash to pay employees and vendors, the business isn’t going to last long.

While profits are important, they can be a lagging indicator. Cash flow, on the other hand, is a real-time reflection of your financial health.

Don’t get caught up in the illusion of profitability on paper – focus on managing your cash flow effectively.

There are many reasons for cash flow problems

Poor budgeting and forecasting

Slow collections from clients

Unexpected expenses and emergencies

Inventory mismanagement

Expanding quickly without a cash flow management plan

While we can’t solve every cash flow problem in one day, we do have a ton of articles about cash flow because it is such an important topic, including:

Here are some key strategies to keep your cash flow healthy:

Embrace the “lean and mean” startup mentality: Especially in the early years, avoid major expenses and prioritize a conservative approach. This doesn’t mean stifling growth; it means being strategic with your resources.

Develop a budget and stick to it: A well-crafted budget is your roadmap to financial health. Track your income and expenses meticulously, and identify areas where you can optimize spending.

Inventory management is crucial: Implement a system to track inventory levels, forecast demand, and avoid overstocking. This prevents unnecessary costs and ensures you have the right products available to meet customer needs.

Consider partnering with an accounting service: A qualified accounting service that fits your vibe can be a valuable asset, especially in the initial years. They can help you set up strong accounting practices, optimize your accounts receivable/payable systems, and ensure you’re on top of your tax obligations.

Other financial threats

Now that cash flow is covered, here is a bit more you’ll want to keep an eye out for in your finances:

Inconsistent Budgeting and Record-Keeping: Without a solid budget and meticulous tracking of income and expenses, it’s difficult to identify areas for improvement or predict potential cash flow challenges.

Tax Neglect:Taxes are a fact of life. Neglecting your tax obligations can lead to hefty penalties and interest charges.

Limited Financial Network: Not building strong relationships with lenders and financial advisors can leave you with limited options when challenges arise. These professionals can provide valuable guidance, access to financing, and help you navigate complex financial situations. Take the time to foster these relationships as soon as possible – you’ll be better equipped to weather financial storms and seize growth opportunities.

Financing Challenges

While cash flow management is crucial, it all starts with having enough financial resources in the first place.

“Of course!” you say.

Doesn’t everybody wish they had a blank check from a wealthy, ethical, no-strings-attached funder?

Well sure, and we’d be happy if you’d give them our number!

But the reality is, many businesses with millions in funding still don’t succeed. A blank check isn’t the answer to everything.

Unrealistic Funding Expectations

Launching a business requires investment.

Whether it’s personal savings, loans, or venture capital, not having enough capital to cover initial expenses and operational costs can hinder your ability to gain traction and establish a strong foundation. Entrepreneurs are often brimming with optimism, but it’s important to have realistic expectations about how much funding you’ll need to get your business off the ground. Underestimating your financial requirements can lead to a funding gap that limits your progress.

For example, if you’re thinking of launching a business that will require significant marketing efforts to succeed, it may be better to wait until you’ve secured enough funding for marketing before taking the leap.

The “lean” method can only take you so far, and it varies wildly based on industry and situation.

Poor Financial Planning

Beyond simply securing funding, a well-defined financial plan is essential. This plan should outline your funding needs, potential revenue streams, and strategies for managing your cash flow.

By carefully considering your funding needs, developing a sound financial plan, and securing adequate resources, you can set your business up for long-term success…with or without that magical blank check!

Operational Efficiency: Streamlining Your Path to Success

Operational efficiency is all about optimizing your processes to achieve maximum results with minimal wasted resources. Here’s how inefficient operations can impact your business:

Wasted Time and Resources: Inefficient processes can lead to wasted time spent on repetitive tasks, unnecessary rework, and underutilized resources. This not only frustrates employees but also translates to lost productivity and higher costs.

Inconsistent Quality: Inefficiencies can lead to inconsistencies in product quality or service delivery. This can damage your reputation and customer satisfaction.

Hindered Growth: As your business grows, inefficient processes become bottlenecks, hindering your ability to scale effectively. Streamlining your operations allows you to handle increased demand and grab those growth opportunities.

Here are some ways to improve your operational efficiency:

Embrace Technology: Automation and digital tools can free up your team’s time for more strategic tasks. Invest in software solutions that automate repetitive tasks, streamline workflows, and improve data analysis.

Standardize Processes: Develop clear and consistent procedures for various tasks within your business. This ensures everyone is on the same page, reduces errors, and improves overall efficiency.

Regularly Analyze and Improve: Don’t settle for the status quo. Regularly evaluate your processes, identify areas for improvement, and implement changes to optimize your operations.

Foster a Culture of Efficiency: Encourage your team to identify inefficiencies and suggest improvements. By empowering your employees and fostering a culture of continuous improvement, you can create a more efficient and adaptable business.

By prioritizing operational efficiency, you can free up valuable resources, improve your bottom line, and position your business for sustainable growth.

Remember, efficiency doesn’t mean cutting corners; it’s about working smarter, not harder.

Focusing on The Customer and Evolving Marketing Trends

“Over 40% of small businesses fail because there’s an insufficient need for their product or service.” – US Chamber of Commerce

The business landscape is dynamic, constantly evolving with new technologies, consumer preferences, and economic shifts.

Business owners need to stay on top of this – just think of how much happened in our world in the last 10 years!

Many businesses lose touch with their audience, assuming their needs are the same as when they first started out.

Others fail to keep their fingers on the pulse of evolving markets, missing out on perfect pivot opportunities and untapped market segments.

Don’t let this be your story!

How to stay relevant and thrive in an evolving marketplace

Embrace Customer Centricity: Put your customers at the heart of everything you do. Gather customer feedback, analyze buying patterns, and adapt your offerings accordingly.

Foster a Culture of Innovation: Encourage a culture of creativity and experimentation within your organization. Invest in research and development, explore new technologies, and actively seek ways to improve your products and services to better meet your customers’ needs.

Stay Agile and Adaptable: Be prepared to change your strategies and business model as necessary.

Business Vision, Strategy, and Execution

A business without a clear vision and well-defined plan can flounder. And even with that, the Founder of EOS Gino Wickman states “Vision without execution is just a hallucination”.

Without a clear strategy, it’s hard to create and measure goals.

Employees might be unsure of their goals and priorities beyond the day-to-day tasks, resulting in frustration, stress, and wasted effort.

And of course, businesses get stuck in reactive decision-making, instead of being able to anticipate what’s needed for their success.

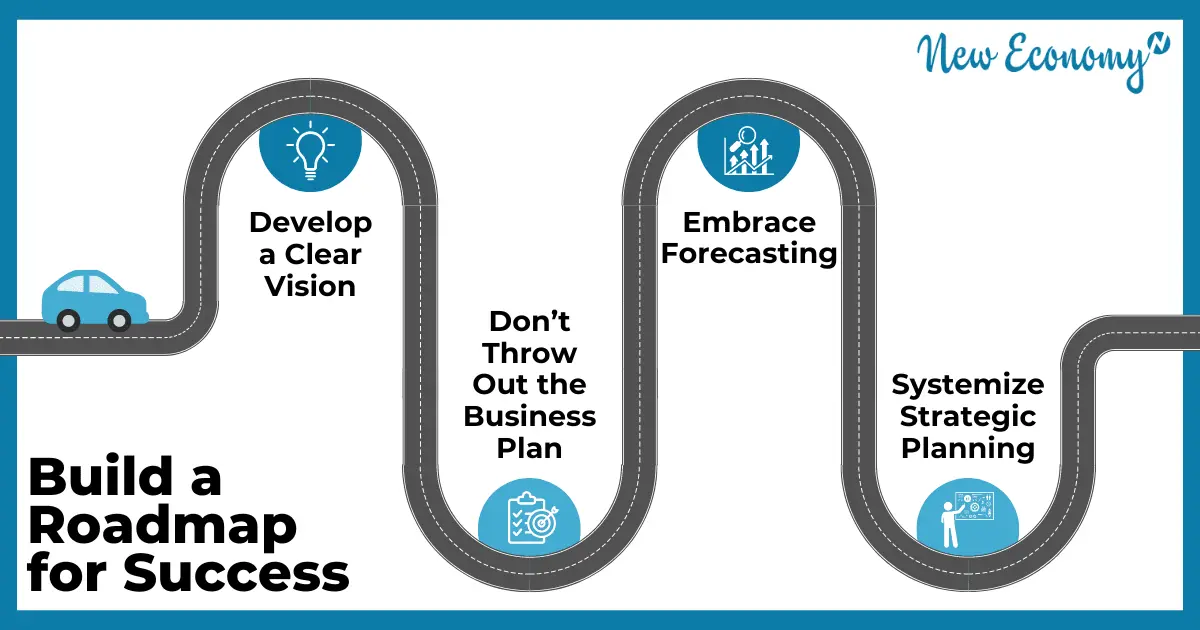

How to Build a Roadmap for Success

Develop a Clear Vision: Clearly articulate your company’s long-term goals and aspirations. What impact do you want to make? What problem are you solving or what need are you fulfilling? A clear vision inspires your team, attracts talent, and guides your strategic direction.

Don’t Throw Out the Business Plan: Business plans aren’t just for the first days of business and getting funding – revisit your plan and adjust it based on what you’re learning.

Embrace Forecasting: Don’t just use your budget as a guide, transform it into a forecast. Some of our customers re-forecast weekly! It’s simply part of their regular weekly process. At New Economy, we do the same.

Systemize Strategic Planning: Make sure you have it in your calendar and are regularly taking the time to update your strategy as needed.

Focus and measure execution: Measure your progress. Hold the team accountable for completing the top priorities in the Strategic Plan.

Other factors

This list isn’t exhaustive. There are countless reasons why a business could fail:

It just means you need to take some deep breaths and put business planning into your calendar as a recurring appointment.

3 Key Takeaways

At New Economy, we help you use financials to make more money and better business decisions so you’ll be in business as long as you want.

Here are 3 key takeaways:

Master Your Cash Flow: Don’t be fooled by profitability on paper. Focus on strategies like budgeting, inventory management, and building strong relationships with lenders and financial advisors to maintain a healthy cash flow.

Embrace Change and Agility: The business landscape is constantly evolving. Stay on top of customer trends, adapt your marketing strategies, and be prepared to pivot your business model as needed. A culture of innovation and customer-centricity is key to staying relevant.

Plan for Success: Develop a clear vision, create a comprehensive business plan, and revisit and revise your strategy regularly. This roadmap will keep your team aligned, focused, and prepared for future challenges.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If identifying ways to decrease your taxes is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting and taxes done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/06/304.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-06-12 15:10:332024-07-02 11:02:42Top Reasons Why Most Businesses Fail After 10 Years and How to Avoid It

The team thinks you’re just one marketing campaign away from surpassing your goals this year.

But can you do it?

How much can you realistically invest in this campaign without jeopardizing other areas of your business?

At New Economy, we use financial data to make nearly every decision.

It’s guided us to the growth we are seeing today.

So, it’s said with confidence and experience when we say:

Without timely and accurate financial data, you can’t answer your business’s most pressing questions.

Of course, intuition has its place.

But fuel your gut with delicious data to ensure your decisions have a foundation for success.

Timely and accurate financial information is the cornerstone of smart business decisions, big or small.

In this article, we’ll explore the reasons why every business, regardless of size or industry, needs up-to-date and reliable financial data to thrive.

Reason #1: Make informed decisions with confidence.

Reason #2: Navigate challenges and opportunities effectively.

Reason #3: Gain a competitive edge and secure funding.

Before we jump in, ask yourself these reflection questions:

Do you feel confident making strategic decisions based on your current financial information?

Are you prepared to react quickly and effectively if a sudden market shift impacts your business?

Have you ever missed out on a potential business opportunity because you lacked clear financial insights?

If you were to seek funding for your business today, are you confident your financial information accurately reflects its true potential?

Ready?

Reason 1: Make Informed Decisions with Confidence

Do you ever feel like you’re navigating your finances in the dark?

At New Economy, we understand how a lack of direction can keep an entrepreneur up at night.

But think of financial data as a compass – guiding your decisions and keeping you headed toward success.

With timely access to your financial information, you can:

Track progress towards goals by measuring how your current performance compares to your budget and identify areas exceeding or falling short of expectations.

Identify areas for improvement by analyzing trends in sales, expenses, and profitability.

Make data-driven decisions instead of relying on guesswork.

Let’s revisit the marketing campaign from the beginning of this article.

By analyzing past marketing data, you can see which strategies brought the best return on investment (ROI).

This allows you to allocate your budget more effectively for the upcoming campaign, maximizing your chances of success

Reason 2: Navigate Challenges and Opportunities Proactively

We all know to expect the unexpected as entrepreneurs!

Whether it’s a global pandemic, supply chain disruptions, or a strangely eventful pop culture event…

there’s no crystal ball to prepare us for the future.

But, smart businesses can still be reasonably prepared for the future with timely and accurate financial data.

It lets you pivot at a moment’s notice.

You can mitigate potential damage or explore a new opportunity with the click of a button if you’ve got the right data on your dashboard.

Here’s how:

By analyzing trends and historical data, you can identify potential financial risks and develop contingency plans to mitigate their impact.

Having a clear picture of your current financial situation allows you to react quickly to unexpected events and adapt your strategies accordingly.

Timely financial data can reveal new market trends or opportunities you might otherwise miss. This allows you to capitalize on these opportunities and stay ahead of the competition.

Now, back to the marketing campaign.

Your sales data starts showing a decline in a specific product category just before launch.

You realize it’s showing a shift in a market trend.

Thanks to the early warning, you can do some research to identify the causes.

Then you can adjust your campaign messaging or even pivot your marketing strategy to target a different product line that’s experiencing higher demand.

Reason 3: Gain a Competitive Edge and Secure Funding

Financial health is a top priority for investors and creditors.

Regardless of the type of funding you seek, your financial health will be reviewed thoroughly before getting anywhere near the purse strings.

Timely and accurate financial data can be a key indicator of your business’s growth potential and ability to repay loans.

Here’s why:

Up-to-date financial statements give a clear picture of your company’s financial performance, profitability, and debt levels. This builds trust with investors.

Financial data can be used to create forecasts and projections for future growth. This allows you to showcase your company’s potential to generate strong returns for investors.

Your funders love when you can answer questions with accurate financial data that was generated recently, instead of bumbling about how they’ll need to wait a few weeks for you to get the data to answer their questions.

A solid understanding of your financial position empowers you to negotiate more favorable terms with lenders and suppliers.

Beyond attracting funding, reliable financial data also helps you stay competitive:

Set competitive prices while maintaining healthy profit margins by analyzing your cost structure and customer behavior.

Gain a clear financial picture to make informed decisions about resource allocation, investments, business expansion, and more.

Let’s come back to our marketing campaign.

You’ve crunched the numbers and decided you just can’t risk dipping into your business savings to launch a massive marketing campaign.

The team decides taking out a short-term, low-interest loan could maximize your outcomes and minimize your risk.

By demonstrating your financial stability and growth potential with accurate data, you’re in a much stronger position to secure funding for the campaign.

When you share how you made your decision to pivot the focus of your marketing campaign based on the most recent data, your funder feels more confident you’re making decisions based on real-world data.

3 Key Takeaways

At New Economy, we want to help you gain control of your finances to make smart decisions.

Part of that is understanding your finances and how to drive business performance.

Here are 3 key takeaways.

Make informed decisions with confidence. Timely and accurate data means you have a more complete picture of your business.

Be prepared for challenges and opportunities. Being able to see your financial records quickly means you can change direction when the time is right.

Secure funding and gain a competitive edge. Showcase your company’s financial position with ease, preparing you for investment, loans, and the ability to gain a competitive advantage.

There you have it 🙂

New Economy Team Members are Experts in Accounting for Entrepreneurs

If collecting timely and accurate data is not in your skill set or you want to gain control of your finances to make smart decisions to build and grow your business, New Economy is an excellent partner.

We’ll help you get your accounting done, and done right.

https://neweconomycpa.com/wp-content/uploads/2024/05/287.png6301200Jeff Allainhttps://neweconomycpa.com/wp-content/uploads/2021/01/new-economy-logo_withpadding.pngJeff Allain2024-05-15 11:43:152024-05-15 11:45:533 Reasons Every Business Needs Timely and Accurate Financial Data